How The Fed Mishandled 40-Year-High Inflation

share

share

share

share

share

share

share

share

share

share

Several months after the US Federal Reserve began describing the country’s inflation problem as “transitory”, the central bank is finally admitting that rapidly rising prices of goods and services are a serious threat to the American economy and its recovery from the coronavirus pandemic.

The problem is the Fed’s response, three modest interest rate hikes by the end of 2022, lifting rates to between three-quarters of a percent to 1%, is woefully inadequate for this level of inflation.

Arguably the Fed has been “behind the curve” from the beginning. It should have foreseen that half a trillion dollars in direct stimulus payments, combined with high demand from a recovering economy set against virus-related supply chain interruptions, would be highly inflationary.

Instead the organization at first denied that inflation was even on the horizon, then said any inflation would be just temporary, transitory, and would end once supply-chain wrinkles were ironed out. Only after the publication of some truly shocking price statistics following Thanksgiving did Fed Chairman Jerome Powell admit that inflation is not actually transitory and that something more serious is going on.

From the press conference following the Wednesday, Dec. 15 Federal Open Market Committee (FOMC) meeting:

“There’s a real risk now, we believe, I believe, that inflation may be more persistent, and that may be putting inflation expectations under pressure, and that the risk of higher inflation becoming entrenched has increased. It’s certainly increased.”

Yet instead of showing that the Fed is serious about controlling inflation, i.e., hawkishly raising rates sooner and higher, Powell and his board of governors have remained dovish, bringing a pea-shooter to an inflation fight requiring a bazooka, a bucket brigade to a raging inferno, pick your metaphor it all points to the same conclusion: the Fed is doing too little too late.

Actual vs Fed inflation

The first thing to understand is that the Fed’s concept of inflation is different from both the official statistic and the reality in the economy. The Consumer Price Index (CPI) is currently 6.8%, which as stated in the headline, is the highest since 1982 — a 40-year high. This is the number most quoted in the financial press; it is the official inflation rate.

But the Fed when it talks about inflation, has since 2012 referred to the “Personal Consumption Expenditures” (PCE) price index. PCE inflation excludes food and fuel, supposedly because they’re too volatile, but the fact that the two most essential price categories are left out, means the Fed is deliberately underestimating true inflation. The central bank reportedly hiked its PCE inflation estimate for 2022 to 2.6% from 2%.

Real “on the ground” inflation is much higher. CPI’s less known but more accurate cousin is the Producer Prices Index (PPI). Unlike CPI, which is crafted by bean counters, the PPI is based on information from actual producers of goods and services. The numbers don’t lie.

The latest PPI data point clocked in at 9.6% for the month of November, year over year — close to double-digit inflation.

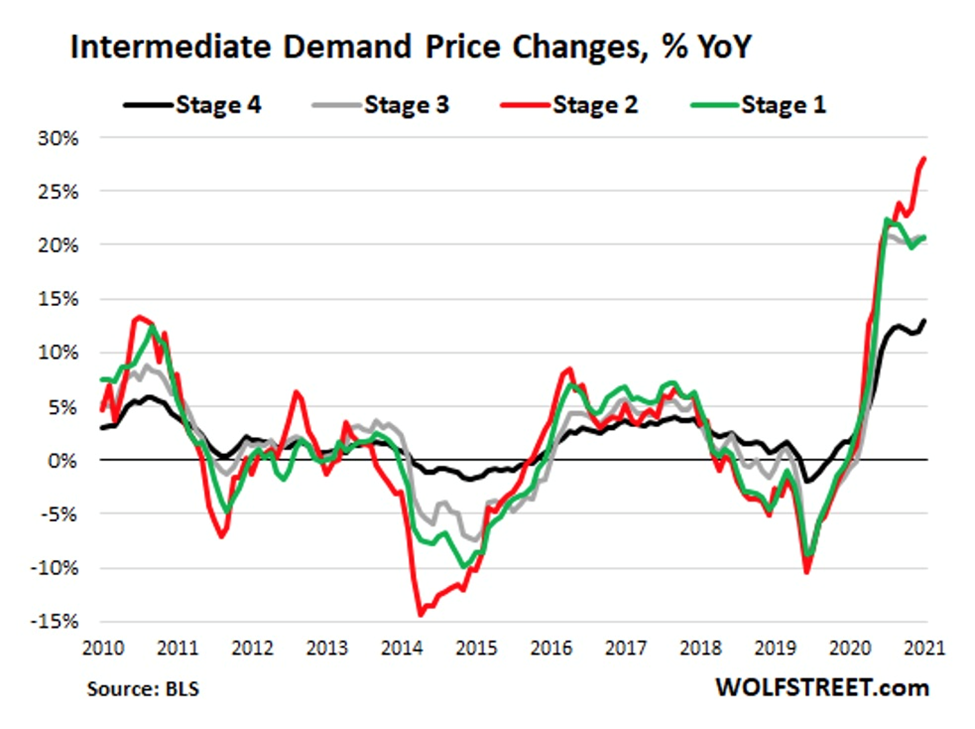

Wolf Street puts more meat on the bones of this statistic, calculating PPI at the various points good are produced. The graph below shows red-hot price increase in the four stages of Intermediate Demand are getting passed onto the next industry in line, and price increases from prior months are now arriving at the Final Demand industries. In Wolf Richter’s words:

At Intermediate Demand Stage 1 industries, furthest up the pipeline, whose production creates the inputs for industries in Stage 2, prices exploded by 20.8% year-over-year (green line), according to the Bureau of Labor Statistics today. At Stage 2 industries, which create the inputs for industries in Stage 3, prices exploded by 28.1% year-over-year, the worst in the data going back to 2010 (red line). At Stage 3 industries, which create the inputs for Stage 4, prices exploded by 20.6% year-over-year (gray line). And at Stage 4 industries, which create inputs to Final Demand, prices shot up by 12.9% (black line):

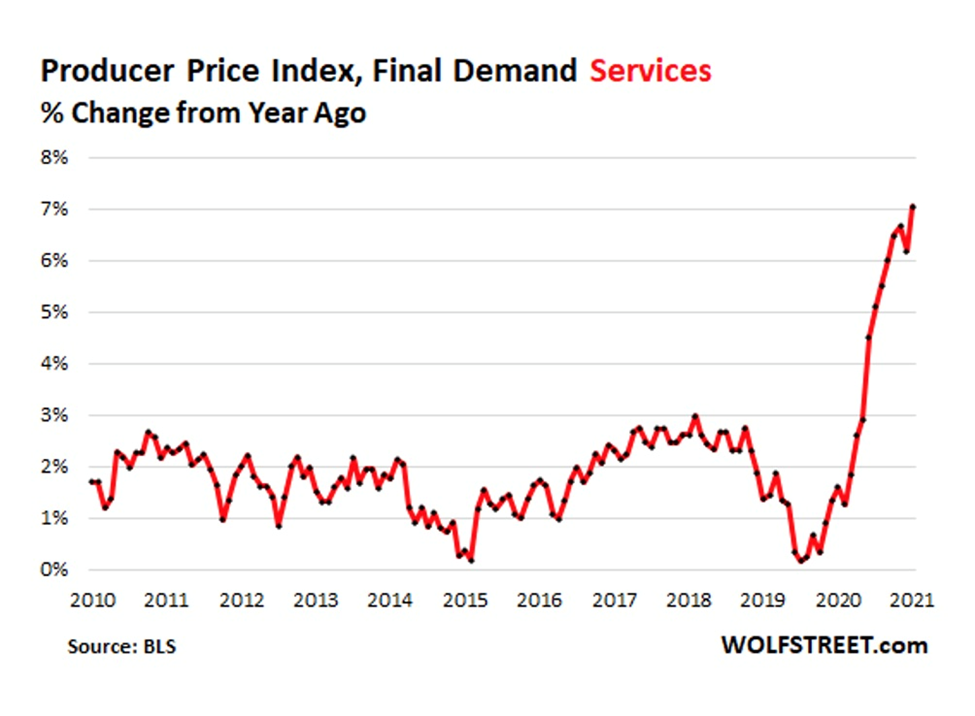

Moreover, inflation has crossed over from goods to services. With Final Demand Services jumping 0.7% in November from October, the 11th month in a row of increases, and 7.1% year over year, the Fed can no longer claim that inflation is only due to goods-related supply chain chaos, semiconductor shortages, shipping container pile-ups, etc.

All the wrong moves

Back to the bucket brigade metaphor, the Fed now realizes that the dumpster fire of inflation has spread to nearby buildings and is furiously chucking buckets of water on it to no avail.

We can see the desperation in how everything is happening that much faster than the last time the Fed tried to quell rising inflation in 2015.

Whereas the Fed slowly began tapering its asset purchases in early 2014 and took five years to run off its balance sheet, the taper this time will take just five months — the FOMC announced this week it will double the speed of the taper to $30 billion a month and end quantitative easing entirely by mid-March instead of June.

The warp-speed taper is due to the strength of the US recovery, what Powell described as “growth above potential”, the unemployment rate falling and “inflation well above target.”

Once QE is ended, the Fed plans to begin raising short-term rates, as stated above, three times in 2022 bringing the target range to between 0.75% and 1% by the end of next year.

Yet it’s still not enough.

“These moves by the Fed amount to little more than spitting into the wind when it comes to taking on inflation,” wrote Peter Schiff in a recent commentary on the Fed’s announced rate hikes. The libertarian and gold bug adds:

“In order to truly take on inflation, the central bank needs to push interest rates at least as high as the inflation rate. Even using the government’s cooked CPI numbers that understate inflation, that would mean taking rates to at least 7%.”

In my opinion the Fed shouldn’t go that far, and I think most others would agree. A 1% rate increase adds about $1,800 per household in interest costs on the $29 trillion national debt. Multiplying that by nine to match the 9.6% PPI inflation rate is clearly impossible as it would wreck the economy.

A more reasonable solution would be to boost the three raises next year say to 1% each, or 1.25%, bringing them within a range of 3% to 4% by year-end 2022. The Fed could even have announced an immediate 1% rate hike this week, to show it was serious about fighting inflation.

Instead, rates are staying at zero for now and we have a very modest set of increases next year that will do next to nothing to reduce inflation. How can a 1% increase at the high end of the range possibly do anything to stop the 9% increase in goods prices and the 7% inflation in services?

Is it any wonder that spot gold shot up immediately following the Fed announcement and continued to climb to an intra-day high of $1,812 on Friday? Silver gained more than a dollar on the news, hitting a three-day high of $22.62 Friday as well.

Source: Kitco

The market needed to hear the Fed was serious about battling inflation and yes that would have dented the stock market temporarily but the spike in precious metals is solid confirmation that the market believes the doves are still in control of the central bank.

Under their leadership, or lack of, inflation has almost hit double digits. Without adequate tightening, and with all the other factors surrounding rising prices including continued supply chain problems, the food and energy crisis and climate change, still happening, they are almost certainly moving higher despite what the Fed says and does.

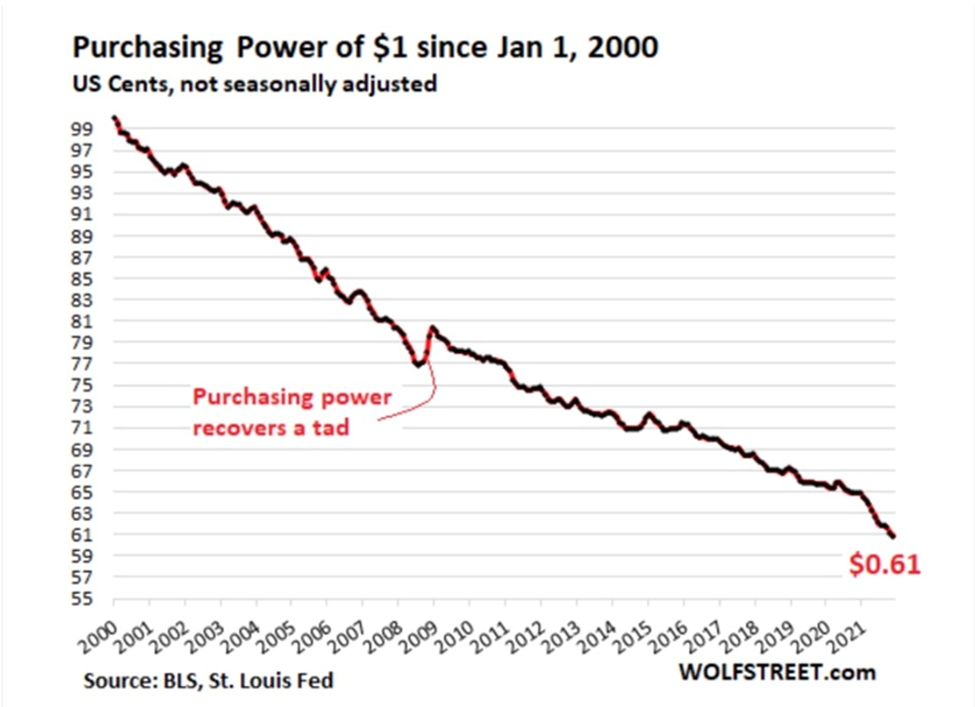

This not only affects prices but purchasing power.

If the actual inflation rate is close to 10%, year over year, how much of your purchasing power has been destroyed?

At AOTH we firmly believe that to protect our investments we need a hedge against inflation and we have always chosen junior gold and silver mining stocks, as historically showing the greatest leverage to rising metal prices.

Among precious metal juniors, it is best in the current inflationary environment to go with pure-play gold and silver companies, which we believe will out-perform. Three of our favorites are Magna Gold, Goldshore Resources and Dolly Varden Silver.

Goldshore Resources (TSXV: GSHR) (OTC: GSHRF) (FRA: 8X00) has embarked on an extensive 100,000-meter drill program on its flagship Moss Lake project that will run until mid-2022.

Earlier this month Goldshore released two more holes from the program, the highlight being a number of higher-grade zones within large, low-grade envelopes. Two main takeaways from the Dec. 8 news release are the significant volume additions and the expanding drill capacity.

According to Goldshore, Mineralization continues to be intersected laterally and at depth, significantly expanding the width and depth of mineralization compared to the 2013 grade model. MMD-21-004 has extended the width and depth of mineralization, relative to the 2013 model, by 38% and 56%, respectively.

The drilling contractor has mobilized two more rigs bringing the total to four, with an additional rig expected to be on site before Christmas.

Results of drilling so far have not disappointed, giving us a glimpse of what may be a significant mineralized system within northwestern Ontario, a historically productive gold-mining province. From the first three holes reported in November, the highlight was hole MMD-21-001, which was mineralized over 550 meters. This corresponds to an estimated true thickness of 422m and a 52% increase over the historical resource model.

Several higher-grade zones were identified including 57 meters at 1.20 g/t Au from 4.0m; 36m at 1.15 g/t from 182m; and 31m at 1.18 g/t from 122m.

The property is located in an excellent jurisdiction with a number of major gold deposits nearby, including Kirkland Lake Gold’s Detour project with 15.7Moz proven and probable reserves at 0.82 g/t Au, New Gold’s Rainy River with 2.6Moz P&P at 1.06 g/t Au, and Cote (IAMGOLD & Sumitomo) with 7.3Moz P&P at 1.0 g/t Au.

Moss Lake itself hosts a number of gold and base metal rich deposits. These include the Moss Lake deposit, the East Coldstream deposit, the historically producing North Coldstream mine and the Hamlin zone, all of which occur over a mineralized trend exceeding 20 km in length.

Goldshore’s Moss Lake project is in northwestern Ontario, a district prized for its gold endowment.

An updated prefeasibility study (PFS) on the property last September showed total proven and probable reserves of 47.6 million tonnes, graded at 0.495 g/t Au, leaving 758,000 ounces of contained gold. Now at full capacity, the San Francisco mine is capable of producing as much as 90,000 ounces annually.

There is also ample room for resource expansion, with an estimated upside of 3Moz gold and 50Moz silver.

Meanwhile, Magna has also been advancing several of its other precious metals assets across Mexico. The next area of exploration focus is Chihuahua, where its newly acquired Margarita silver project is situated. The project is a low-intermediate sulfidation epithermal Ag-Pb-Zn system, which can be traced to many of Mexico’s producing silver mines.

Drill programs are also planned at the San Judas and Veta Tierra gold projects, and the La Pima silver project.

Situated within a region mostly known for its vast copper and gold resources, Dolly Varden Silver Corp. (TSXV: DV) (OTC: DOLLF) is uniquely positioned as a pure silver miner exploring the Golden Triangle of British Columbia.

The company’s flagship and namesake project hosts four historically active silver mines, including two past-producing deposits with a combined silver production of 20 million ounces between 1919 and 1959.

The exploration focus is currently on expanding the high-grade silver resource at the Torbrit deposit, which accounted for most of the historic production (19Moz), and finding potential Torbrit “look-alikes” along a trend that stretches over 4.5 km.

The ultimate goal is to advance Dolly Varden to be the next high-grade pure silver mine in this prolific mining region.

The Dolly Varden property lies to the west of Hecla Mining’s (NYSE: HL) Kinskuch property, an early-stage project with potential for discovery of epithermal silver-gold, gold-rich porphyry and VMS deposits.

But the ultimate focus is still silver, given that Dolly Varden is the largest pure-play silver project in all of Canada.

DV is currently in the midst of an aggressive two-year drilling campaign designed to expand the existing silver resource of the Torbrit deposit and to test multiple highly prospective targets on the property. The initial surface diamond drill program consists of 10,000 meters.

For over two years, the company has been updating the resource model with drilling to bolster its understanding of the existing resource, so that it can easily target specific areas of the deposit for conversion from inferred to indicated/measured resource categories.

This year’s drilling at Torbrit will focus on areas within the updated block model where a high percentage of inferred resources exist, and where the higher silver grade blocks are at the outer edges of the model.

As we’ve previously discussed, DV effectively has a two-pronged approach to increasing shareholder value. Not only could it grow the Dolly Varden resource base through more drilling, but the company could also go a step further by acquiring neighboring properties.

Earlier this month, DV made its biggest move yet by acquiring the Homestake Ridge gold-silver property from Fury Gold Mines in a transaction valued at C$50 million. The Homestake property covers a 7,500-hectare land package contiguous to and northwest of the Dolly Varden property.

Homestake currently hosts an estimated resource of 165,993 oz gold and 1.8 million oz silver in the indicated category, plus 816,719 oz gold and 17.8 million oz silver inferred.

To date, more than 275 holes for over 90,000m of drilling have been completed on the Homestake property; multiple exploration targets remain to be tested along a combined 15 km strike length.

Following the transaction, Homestake and Dolly Varden will be amalgamated to form one single project known as Kitsault Valley, with a combined mineral resource base of 34.7Moz silver and 166,000 oz gold indicated and 29.3Moz silver and 817,000 oz gold inferred.

This combination would solidify DV’s Kitsault Valley project as among the largest high-grade, undeveloped precious metal assets in all of Western Canada.

Conclusion

I disagree with Peter Schiff in how high the Fed should raise interest rates to fight inflation but I agree with him in that if the central bank was serious about fighting inflation it would have started the war long ago.

The evidence was overwhelming a year ago that there was an inflation problem yet the Fed did nothing and continued to insist it was transitory. A simple calculation from a previous article showed that $3,200 “stimmy” payments to 169 million Americans would result in half a trillion dollars added to the real economy, a good portion of which would be spent, resulting in inflation. This along with the supply chain interruptions from covid, the spike in fuel prices (natural gas and crude oil), lumber, and climate change-related price increases to agricultural commodities and food, should have all been red flags signaling a hawkish policy response was needed.

Instead, nothing was done, the situation is now serious, yet the Fed is still acting as though inflation is no big deal.

The sad part in all of this is the people who will be hurt most are the poor and the downtrodden. Forced to pay higher grocery prices, more expensive electricity, more at the pump, they are the ones most likely to be evicted, to have to go on food stamps, to need to choose between feeding their kids and clothing them. Read more about the coming American spring

The Fed has utterly failed in its mandate to control inflation and have nobody but themselves to blame. They were behind the curve from the beginning, all they needed to do was add two plus two but they were incapable of even doing that. We are stuck with inflation, high prices and the destruction of consumers purchasing power.

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

Richard does not own shares of Goldshore Resources (TSXV: GSHR), Magna Gold (TSXV: MGR) or Dolly Varden Silver Corp. (TSXV: DV). GSHR, MGR and DV are paid advertisers on Richard’s site aheadoftheherd.com

*********

share

share

share

share

share