Applied Rorschach

share

share

share

share

share

share

share

share

share

share

Way back in 1921, a heretofore unknown Swiss psychologist by the name of Hermann Rorschach developed a test to examine the human mind in a manner which could be thought of as “a psychometric examination of pareidolia, the active pattern of perceiving objects, shapes, or scenery as meaningful things to the observer's experience, the most common being faces or other pattern of forms that are not present at the time of the observation” (Wikipedia). Now, I will not go into the minutiae surrounding this application of folded ink blots to human behaviour but I will tell you why it has arrived as the dominant theme for the weekly missive. I was listening to a number of interviews with various world-renown economists and market mavens in which this raging (and very irritating) debate over the inflation/deflation prognosis was being batted back and forth using all kinds of historical precedents, charts, and ratios all designed to bestow credibility and the far more important authority upon the proponent of the case. With both sides arguing the ink blot opposite views on essentially the same data, it reminded me of the Rorschach Test where two people can look at the same image and see something completely different.

As completely fitting as it is here in the final throes of 2021, investors are desperately trying to determine whether 2022 will usher in a continuation of record highs in stocks along with record highs in “stuff” like copper, natural gas, oil, iron ore and the far more significant “softs” like grains, meats, and fibres (like cotton) – or – whether this well-advertised shift in Fed policy will cause dual reversals. The reason that the Rorschach image popped into my head was my visualizing a forty-year trend of disinflation where bond yields have declined, P/E multiples expanded, bubbles popped then resurrected by Fed interventions, and finally the creation of an entirely new class and age of investors that have never endured anything vaguely resembling a bear market with the exception being a very brief four-week decline in March/2020. That represents the ink blot on the bare page and when you fold the paper at the extreme right edge of that image and press down firmly, what appears when you open up the sheet of paper is the image shown at the start of this missive.

If the primary driver of all of those financial asset tailwinds was deflation, then does it not stand to reason that the removal of same should (and will) result in an equal and opposite reaction? Stated another way, how can the stock and housing bulls maintain their bullish behaviours given the absence of the primary driver (deflation)?

The difficulty in investing these days lies in one simple reality: with central banks and sovereign treasury departments hitting the stimulus panic buttons at the slightest sniff of a 2-3% stock market swoon, they have created an entire generation of Pavlovian mouse-clickers leaping into action, bidding up stocks with hair-trigger efficiency and blind enthusiasm. Sadly, older investors such as me that have been unable to “get it” since the Great Financial Bailout of 2008 that saved billionaire bankers while burying the taxpayer (and millions of homeowners) which also marked the dawn of an era that has since been branded as the “Everything” bubble. Make no mistake, the youngsters have been right and the dinosaurs wrong for over twelve years but the problem is that asset price inflation (or shall I say bank collateral inflation) has now met up with rising consumer price inflation. Celebration over the value of the Millennial stock portfolio is accelerating into anger over the escalation of everyday expenses and where the rubber meets the road and the Louisville Slugger meets the banker’s skull is where the cost of that Starbuck’s grande latte rises faster than the Tesla call options they bought (that expire next week).

I get a distinct premonition that the landscape is changing and that the time for definitive action is drawing nigh. What worked since 2008 did so in a period of relative calm in both consumer prices and labour markets. Despite massive monetary (and now fiscal) stimulus, the only raise that Joe Sixpack needed was the one his portfolio got every time he heard Jerome Powell tell him to “buy the dip cuz the Fed’s got yer back” while cheap goods being brought to the West from the foreign labour camps softened the impact of consumer price increases on the psyche of the American (and western) investor.

When I was learning my trade back in the early 1980’s, it was pounded into my head that stock prices were to be seen as a barometer of economic activity. Today, Fed officials and the politicians would have us believe that stock prices are a thermometer and that rising prices represent a gauge signalling the relative health of the economy. That notion dissolves into nothingness when it is revealed that an entity called the “central bank” can use a phony account to buy anything they want and in any amount. It renders the action in stocks and gold and bonds and currencies as nothing more than a video game. No longer do the emotions of fear and greed dictate price movements and there is no better illustration than in gold and silver, where for centuries they assume safe haven roles with dignity and unanimity.

In discussion with a colleague on Friday (who for years ran a large trading desk in Toronto for one of the biggest investment dealers on the planet), he informed me that the traders he speaks to dozens of times each week and who all swoop and dive into the same sectors once trends have been established all think that the markets here in 2021 are totally and completely “broken”. Thanks to this serial interference by the banks (all sanctioned and cheer-led by their respective central bank or government), the fluidity with which markets once functioned is gone. “Try and sell 500,000 shares of anything these days and the computer algorithms cancel every big in the stack.” He also opined that “if you had told me three years ago that in December 2021, we would have a 6.8% CPI, I would have bet my BMW on a $2,500 gold price.”

Every place I look in the world of money, there lies the DNA of Fed intervention and interference. Their fingerprints and bodily fluids are found everywhere – in the mainstream media, in all markets, and in all countries. When the prices for gold and silver are treated as “national security concerns”, they are by default positioned directly opposite the power and authority of the U.S. government and since the U.S. is both the policeman and the head policy-architect for the G20 nations, you have what amounts to a consortium of anti-gold/silver conspirators making sure that they are never allowed to be seen as “canaries in the methane-filled coal mine”. Those birds were dead long ago and the fabricated cheeps you hear coming from the mine are about as real as “transitory inflation”.

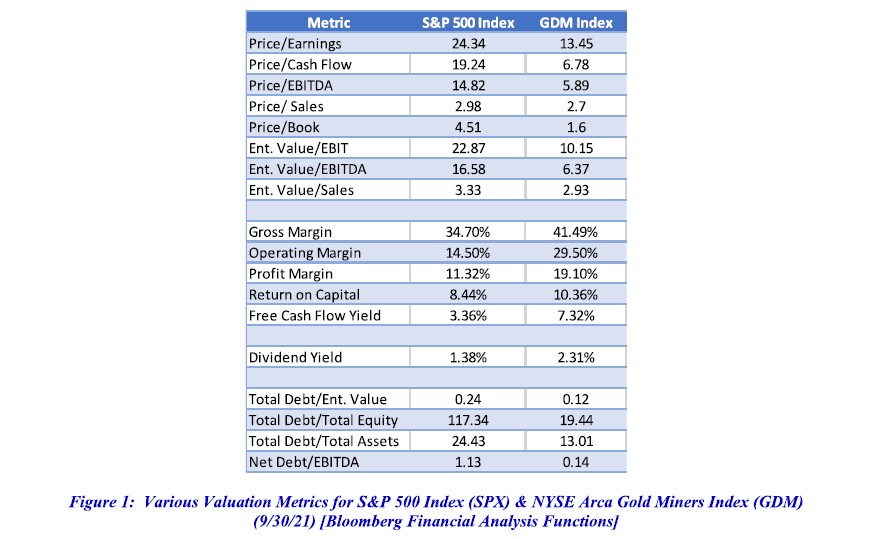

The only charts to show this week are the two that reside in deep contrast to the table created by Trey Reik and posted here a couple of weeks ago. I start with the fundamental snapshot of comparison between the gold and silver mining companies domiciled in the GDM Index and the S&P 500 component companies

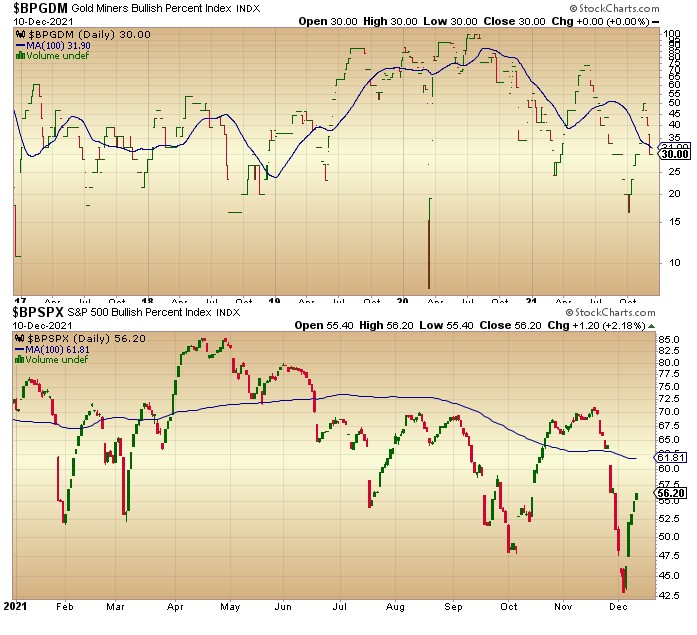

Now look at the “Bullish Percent Index” for the S&P and the GDM. This index measures the percentage of stocks currently rated as “BUYS” through point-and-figure analysis so when you consider that 56.20% of all stocks found in the S&P 500 are on P&F “BUYS” versus 30% for their GDM counterparts, it reeks of a total disconnect in market efficiency.

If markets are understood to represent all of the collective wisdom, experience, sentiment, and skillsets of vast assortments of human beings around the world, how on earth with all of our supercomputers armed with advanced software, artificial intelligence, and pattern recognition technology can there be such a disconnect? In my view, it goes right back to the Fed and its masterful job of thought control as the younger legions of investors have never made any serious money in gold and silver (certainly nothing compared to tech, crypto, and cannabis). Take the analogy of the cat jumping up in a hot stove; it only happens once because if there is one sensation that triggers perfection in the rote memory process, it is pain and since there has been a distinct absence of pain in owning tech stocks and distinct preponderance of pain in owning resource stocks, it stands to reason that the optimal driver for my beloved miners is the arrival of pain for everyone else. The horror of such an attitude is that while I generally wish that everyone could enjoy the fruits of their labour in the process of selecting suitable investments, those people that have been correct in their assumptions on inflation and commodity prices (including gold and silver) have not been rewarded with any resembling a commensurate return for their hard work.

Heading into the final two weeks of the year, the first sign of light in what has been a very long and dark tunnel for the vast majority of precious metals investors arrived in the form of a long-awaited bid for Great Bear Resources Ltd. (GBR:TSXV)(CAD $28.55). This is the kind of reward that has been so fleeting for the junior resource investors largely because major mining companies have had a horrific track record since 2001 in their acquisitions. In fact, Kinross buying GBR triggers memories of their 2009 ill-fated $139 million takeover of Yukon explorer Underworld Resources which was written off to zero by 2016. Iamgold’s takeover of Trelawney in 2012 for over CAD $600 million (later put on “Care and Maintenance”) and Pan American Silver’s $630 million acquisition of Aquiline’s Navidad silver project (still dormant due to permitting problems) are further examples of exactly why the major miners have been in the institutional doghouse since 2011. I am looking to the heavens and praying that the Dixie Project becomes a serious value-driver for Kinross and that it works out for J. Paul Rollinson better than it turned out for Tye Burt.

The Kinross-Great Bear transaction gives me great comfort that the cycle that has eluded us despite what has appeared to be a near-perfect storm for gold and silver investors. What I want to see is a massive move in the senior miners or a massive allocation shift by generalist portfolio managers (or both) that allows them unbridled flexibility to use inflated paper to acquire every developer on the planet with a) undervalued resources and b) exploration upside which are both very much a characteristic of my largest holding and top pick, Getchell Gold Corp. (GTCH:CSE / GGLDF:US OTC QB) and where leverage is the name of the game.

*********

share

share

share

share

share

More from Silver Phoenix 500