The Big 8 Increase Their Short Position in Silver

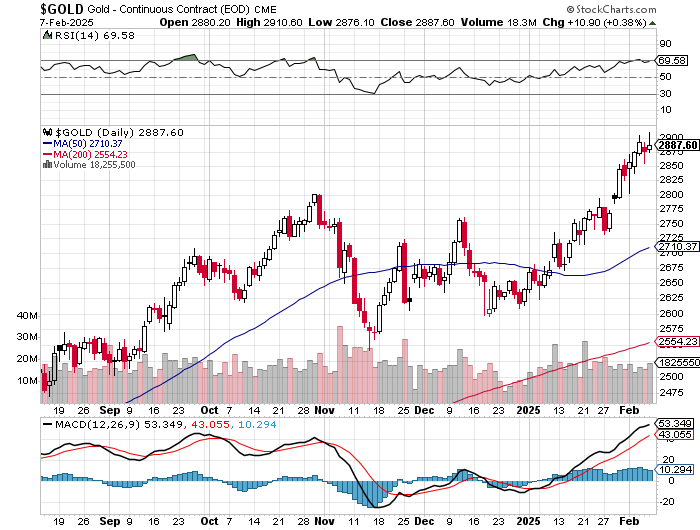

The gold price took two broad and somewhat uneven steps higher in early Globex trading on Friday -- and that was allowed to last until around 9:10 a.m. in London. From that juncture it was sold quietly lower at an ever-increasing rate until a minute or so after the non-farm payroll number came out at 8:30 a.m. in COMEX trading in New York. About thirty minutes after that it began to rally rather sharply until 'da boyz' showed up with all guns blazing at 10:45 a.m. EST -- and backed by a spike in the DXY that began about five minutes later. It was then engineered lower until 12:35 p.m. -- and from that point it struggled quietly higher until about forty or so minutes before trading ended at 5:00 p.m. EST.

The high and low ticks...both of which were set in COMEX trading in New York...were recorded as $2,910.60 and $2,876.10 in the April contract...an intraday move of just under 35 bucks. The April/June price spread differential in gold at the close in New York yesterday was $26.30...June/ August was $25.20...August/October was $25.40 -- and October/December was $25.20 an ounce.

Gold was closed in New York on Friday afternoon at $2,860.10 spot...up only $4.70 on the day -- and $25.50 off its Kitco-recorded high tick. Net volume was on the heavier side for the first time in a while, at around 177,000 contracts -- and there were around 18,500 contracts worth of roll-over/switch volume out of April and into future months in this precious metal...mostly June and August.

I saw that 1,808 gold, plus 172 silver contracts were traded in February yesterday, so we'll see what that translates into in tonight's Daily Delivery and Preliminary Reports.

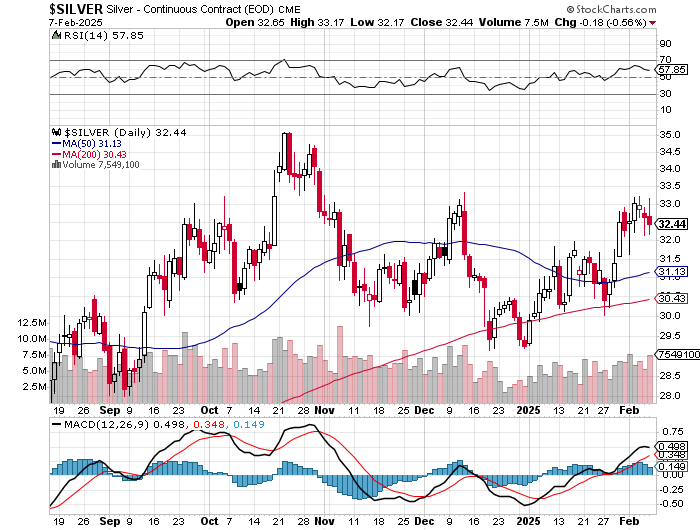

Silver's two broad and quiet rallies in early Globex trading were dealt with in the usual manner -- and once the noon silver fix was done in London, it was sold lower until the non-farm payroll number showed up at 8:30 a.m. in COMEX trading in New York. Its ensuing rally met the same fate as gold's rally at exactly the same time...minutes after 10:30 a.m. EST...except they leaned on its price until around 3:31 p.m. in after-hours trading -- and it recovered about a dime after that until the market closed at 5:00 p.m. EST.

The high and low ticks in silver, both of which were set in New York, were reported by the CME Group as $33.165 and $32.175 in the March contract...an intraday move of 99 cents. The March/May price spread differential in silver at the close in New York was 31.0 cents...May/July was 29.5 cents -- and July/ September was 29.9 cents an ounce.

Silver was closed in New York on Friday afternoon at $31.785 spot...down 41 cents on the day -- and a whopping 84.5 cents off its Kitco-recorded high tick. Net volume was a touch on the heavier side at 61,000 contracts -- and there were a bit under 19,000 contracts worth of roll-over/switch volume out of March and into future months in this precious metal...mostly May, but with noticeable amounts into July and September as well.

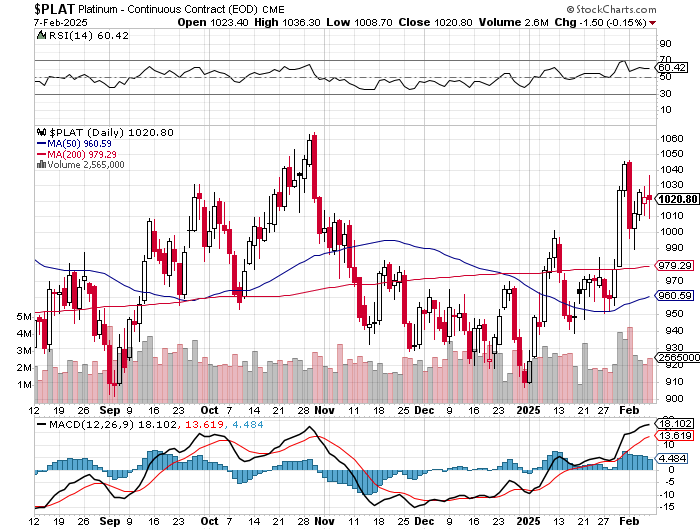

Platinum had a broad up/down move that lasted until the 2:15 p.m. afternoon gold fix in Shanghai. Its ensuing sharp rally ran into the short sellers of last resort around 10:40 a.m. in Globex trading in Zurich -- and its second rally ran into them again around 9:25 a.m. in COMEX trading in New York. They engineered it unevenly lower from that point until minutes before 4 p.m. in after-hours trading -- and about an hour later, jumped a few dollars higher until trading ended at 5:00 p.m. EST. Platinum was closed at $974 spot...down 12 bucks from Thursday -- and 23 dollars off its Kitco-recorded high tick.

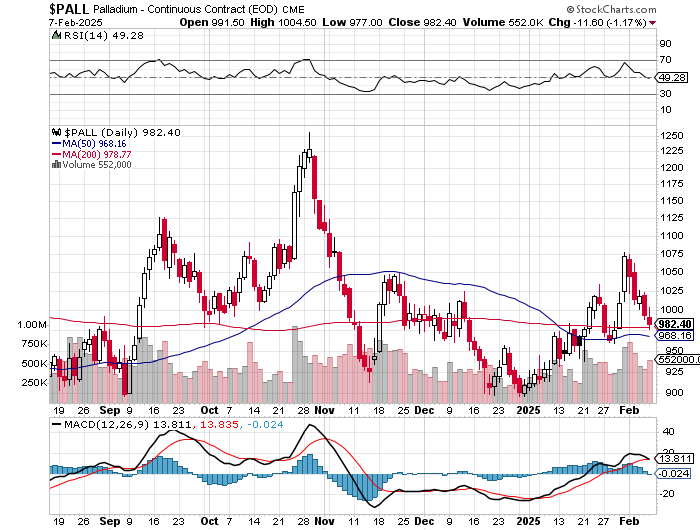

Palladium's price path in early Globex trading was a more subdued version of platinum's up until around 10:45 a.m. in Zurich. 'Da boyz' appeared in at that juncture, setting it low tick around 8:40 a.m. in New York -- and from there its ensuing rally ran into 'grief' once again around 11:35 a.m. EST -- and from that point it was engineered lower until it touched its previous low tick at the 5:00 p.m. EST close. Palladium was closed at $950 spot...down a further 14 dollars -- and 22 dollars off its Kitco-recorded high tick.

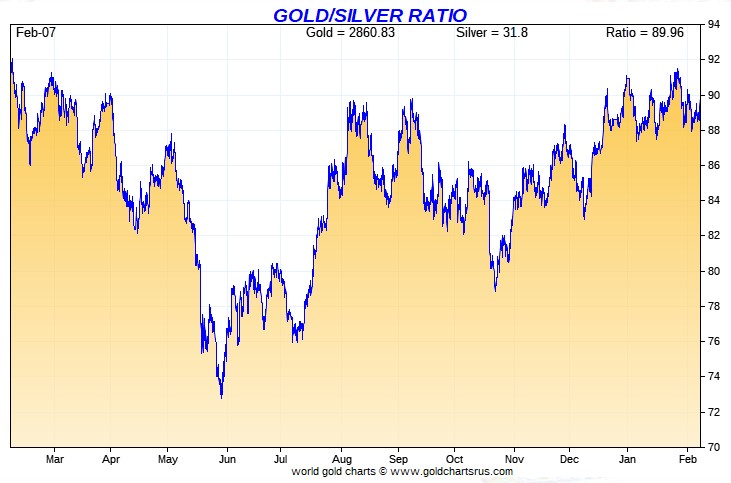

Based on the kitco.com spot closing prices in silver and gold posted above, the gold/silver ratio worked out to 90.0 to 1 on Friday...compared to 88.7 to 1 on Thursday.

Here's the 1-year Gold/Silver Ratio Chart...courtesy of Nick Laird. Click to enlarge.

--------

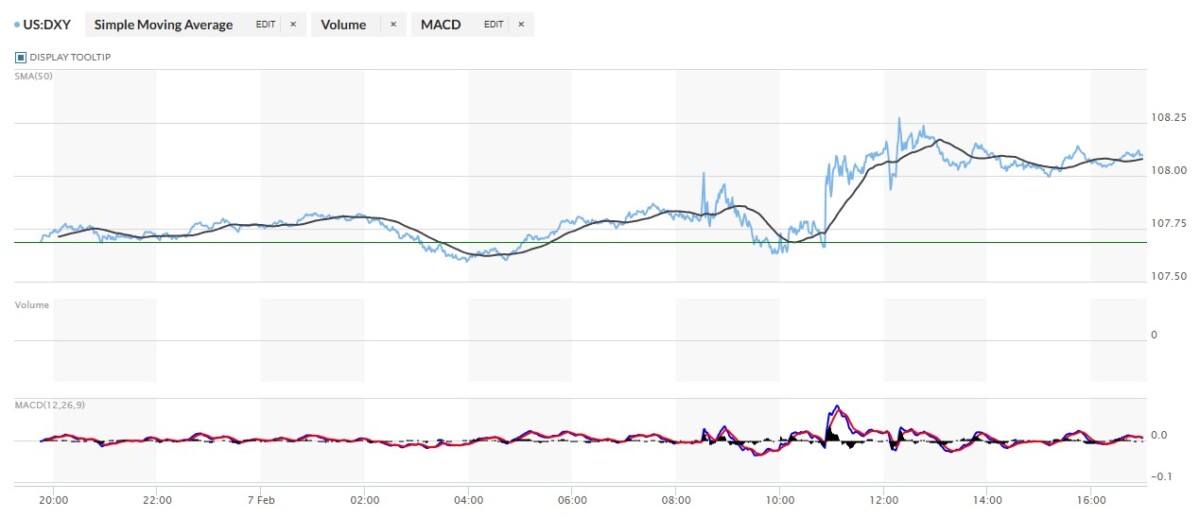

The dollar index closed very late on Thursday afternoon in New York at 107.69 -- and then opened exactly unchanged once trading commenced at 7:45 p.m. EST on Thursday evening...which was 8:45 a.m. China Standard Time on their Friday morning. It chopped quietly higher until around 2:03 p.m. CST. About an hour later a broad and quiet down/up move began that lasted until around 12:33 p.m. in London. It had a quick up/down move at the 8:30 a.m. jobs report in Washington...edged higher until 8:55 a.m. -- and then headed lower until 9:50 a.m. It didn't do much from that point until it spiked up a bit starting at 10:50 a.m. EST, with its spike 108.27 high tick set at 12:18 p.m. It then had an uneven and slightly descending down/up move centered around 3:12 p.m. that lasted until the market closed at 5:00 p.m. EST.

The dollar index finished the Friday trading session in New York at 108.04...up 35 basis points from Thursday's close -- and 6 basis points below its indicated close on the DXY chart below.

Here's the DXY chart for Friday...thanks to marketwatch.com as usual. Click to enlarge.

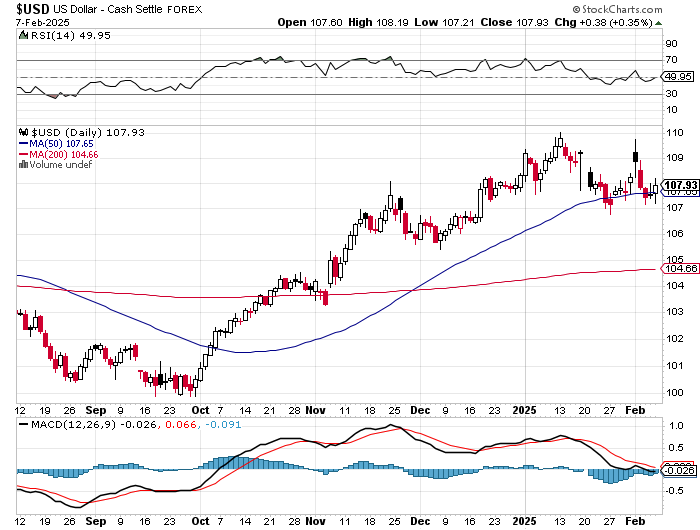

Here's the 6-month U.S. dollar index chart...courtesy of stockcharts.com as always. The delta between its close...107.93...and the close on DXY chart above, was 11 basis points below that. Click to enlarge.

'Da boyz' ramped the DXY about five or so minutes after the set the high tick gold -- and about 15 minutes after that in silver. The DXY 'rally' was just as engineered as the price declines in both silver and gold. The price action in platinum and palladium, including their respective high ticks, were totally uncorrelated with what was happening in the DXY.

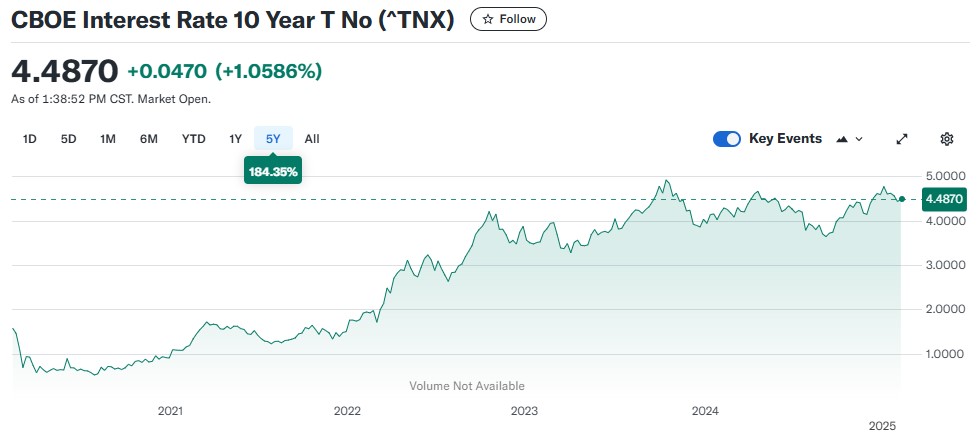

U.S. 10-year Treasury: 4.4870%...up 0.0470/+(1.06%)...as of the 1:59:52 p.m. CST close

The 10-year closed lower by 8.2 basis points on the week...courtesy of the Fed.

Here's the 5-year 10-year U.S. Treasury chart from the yahoo.com Internet site -- which puts the yield curve into a somewhat longer-term perspective. Click to enlarge.

As I continue to point out in this spot every week, the 10-year hasn't been allowed to trade above its 4.92% high tick set back on October 15, 2023 -- and it's more than obvious from this chart that it will he held at something under 5% until further notice.

-------

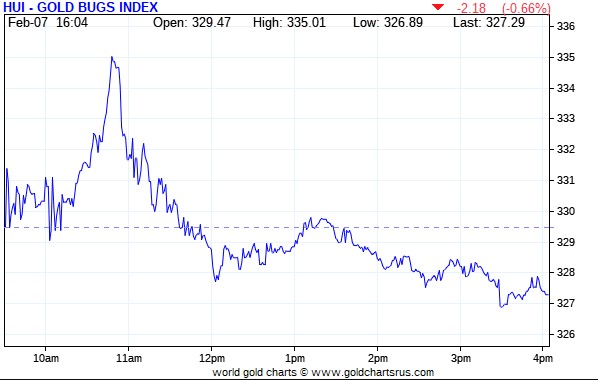

Although the gold price began to rally sharply starting around 9:05 a.m. in New York...its associated equities didn't get the message until around 10:15 a.m. Then they jumped up a whole bunch until that ramp job in the DXY appeared -- and it was pretty much all down hill from that juncture until 3:30 p.m. They didn't do much after that. The HUI closed down 0.66 percent.

Not surprisingly, the silver stocks didn't do as well. Nick Laird's 1-year Silver Sentiment Index closed down 1.69 percent. Click to enlarge.

The two 'stars' were Aya Gold & Silver -- and SilverCrest Metals...closing up on the day by 0.41 and 0.09 percent respectively. The biggest dog amongst many was Endeavour Silver, down 4.16 percent...maybe on this news.

Except for the above news from Endeavour Silver, I didn't see any news yesterday on any of the other now twelve silver companies that comprise the above Silver Sentiment Index.

The index is about to get cut down to eleven silver companies once Coeur Mining completes its takeover of SilverCrest Metals on or about February 14.

The silver price premium in Shanghai over the U.S. price on Friday was 6.23 percent.

The reddit.com/Wallstreetsilver website, now under 'new' but not improved management, is linked here. The link to two other silver forums are here -- and here.

-------

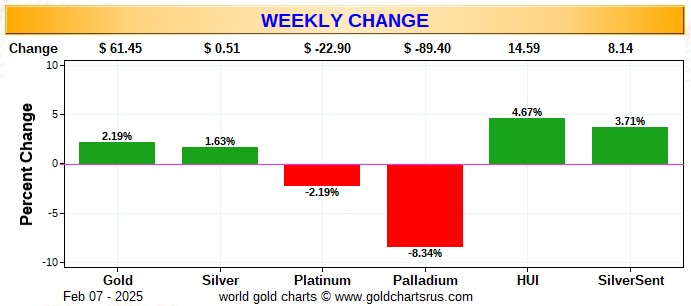

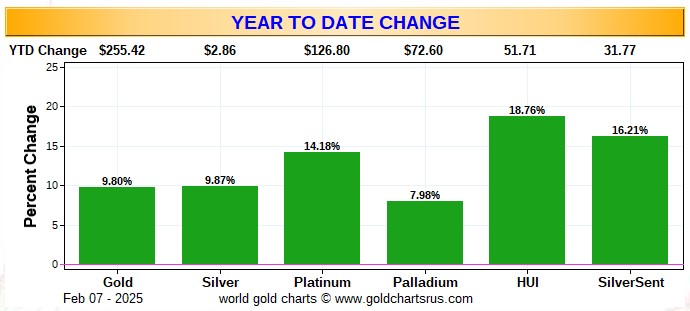

Here are two of the usual three charts that appear in this spot in every weekend missive. They show the changes in gold, silver, platinum and palladium in both percent and dollar and cents terms, as of their Friday closes in New York — along with the changes in the HUI and the Silver Sentiment Index.

Here's the weeklychart...which doubles as the month-to-datechart for this one week only -- and I'm just happy that it's green across the board once again. The only reason that everything silver related didn't outperform everything gold related is because of the lickin' 'da boyz' laid on silver on Friday. Click to enlarge.

Here's the year-to-date chart -- and I'm also happy that it's green across the board -- and like for the weekly/month-to-date chart, silver is underperforming relative to gold, only because of the lid that the Big 8 commercial short have on it. Click to enlarge.

Of course -- and as I mention in this spot every Saturday -- and will continue to do so...is that if the silver price was sitting close to a new all-time high of $50+ dollars an ounce, like gold is now back at its nominal all-time high of $2,800+ the ounce...it's a given that the silver equities would be outperforming their golden cousins...both on a relative and absolute basis -- and by a country mile.

------

The CME Daily Delivery Report for Day 6 of February deliveries showed that 2,550 gold -- and an unexpected zero silver contracts were posted for delivery within the COMEX-approved depositories on Tuesday.

In gold -- and like I've done since First Day Notice, I'm not going to attempt to itemize the huge list of short/issuers and long/stoppers...as they are myriad, especially the number of long/ stoppers. Suffice to say that in the Big 4/8 commercial category...all the world's bullion banks are fully represented once again...except for French bank BNP Paribas.

The link to yesterday's Issuers and Stoppers Report is here.

Month-to-date there have already been a record 55,127 gold contracts issued/reissued and stopped -- and in silver, that number is 3,327 contracts. In platinum it's 587 contracts -- and in palladium...8.

The Preliminary Report for the Friday trading session showed that gold open interest in February dropped by 1,724 COMEX contracts, leaving 8,651 still open...minus the 2,550 contracts out for delivery on Tuesday as per the above Daily Delivery Report. Thursday's Daily Delivery Report showed that 2,112 contracts were actually posted for delivery on Monday, so that means that 2,112-1,724=388 more gold contracts were added to the February delivery month.

Silver o.i. in February fell by 492 COMEX contracts, leaving 466 still around. Thursday's Daily Delivery Report showed that 580 silver contracts were actually posted for delivery today...so that means that 580-492=88 more silver contracts just got added to February deliveries.

Total gold open interest on Friday decreased by 1,170 contracts -- and total silver o.i. took a big hit...dropping by 4,516 COMEX contracts. I was certainly happy to see that.

[I checked Thursday's final total open interest numbers -- and the change from the Preliminary Report in gold showed a decrease, from -5,909 contracts ...down to -6,297 contracts...the more the better, as always. Final total silver o.i. rose by an insignificant amount...from +156 contracts, up to +183 contracts.]

I saw that gold open interest in March dropped by 1 contract yesterday. Open interest in that month is 14,728 COMEX contracts...which is enormous for a non--scheduled delivery month.

-------

After no change in GLD on Thursday, an authorized participant added 138,406 troy ounces of gold to it on Friday -- and there were also 17,831 troy ounces of gold added to GLDM. And after several weeks of straight withdrawals from SLV, an a.p. added 1,821,028 troy ounces of silver to it on Friday.

The last SLV borrow rate late on Friday showed 13.27% -- and 150,000 shares available...up from 12.16% earlier in the day. The last GLD borrow rate was 4.73%...with 1,000,000 shares available...down from 6.29% earlier in the afternoon.

In other gold and silver ETFs and mutual funds on Planet Earth on Friday, net of any changes in COMEX, GLD, GLDM and SLV activity, there were a net 106,529 troy ounces of gold added -- and a net 2,243,653 troy ounces of silver were added as well...the lion's share of which were the 2,210,788 troy ounces that were deposited at iShares/SSLN.

And still nothing from the U.S. Mint.

------

It was yet another huge day in gold deliveries over at the COMEX-approved depositories on the U.S. east coast on Thursday, as 734,773 troy ounces were received -- and nothing was shipped out.

In the 'in' category, there were six depositories involved. The two largest were Brink's, Inc. and JPMorgan...receiving 385,812.000 troy ounces/12,000 kilobars -- and 192,906.000 troy ounces/6,000 kilobars respectively.

There was decent paper activity...starting off with the 96,679 troy ounces transferred from the Registered category and back into Eligible over at Malca-Amit USA. The remaining 24,113.250 troy ounces/750 kilobars and the 16,011.198 troy ounces/498 kilobars were transferred from the Eligible category and into Registered over at Manfra, Tordella & Brookes, Inc. and Brink's, Inc. respectively.

The link to Thursday's considerable COMEX gold action is here.

The silver action was just as impressive, as 2,637,949 troy ounces were reported received -- and nothing was shipped out.

The largest 'in' amount were the 1,459,586 troy ounces received at Brink's, Inc...with the remaining 1,178,363 troy ounces/two truckloads arriving at JPMorgan.

There was considerable paper activity as well...with 1,909,901 troy ounces/ 382 COMEX contracts worth...getting transferred from the Eligible category and into Registered over at Brink's, Inc. -- and no doubt going out for immediate delivery.

The link to all of Thursday's considerable COMEX silver action is here.

And it was also exceptionally busy over at the COMEX-approved gold kilobar depositories in Hong Kong on their Thursday...all of it at Brink's, Inc. as usual. They reported receiving 1,351 kilobars -- and shipped out 4,954 of them. The link to this, in troy ounces, is here.

The Shanghai Futures Exchange reported that a net 377,870 troy ounces of silver were added to their inventories on their Friday, which now stands at 45.968 million troy ounces.

------

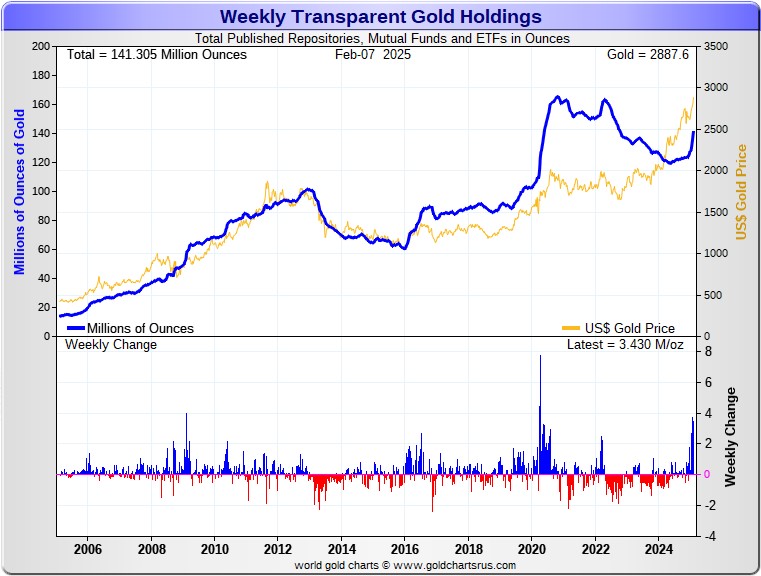

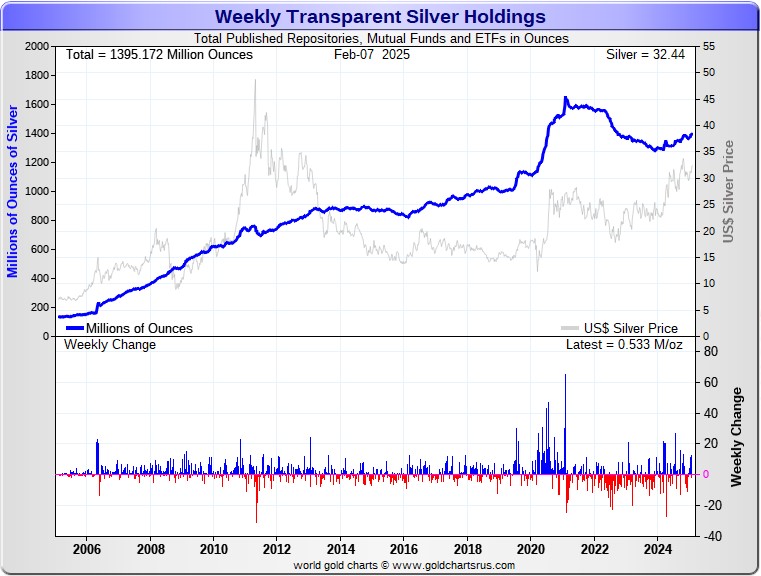

Here are the usual 20-year charts that show up in this space in every weekend column. They show the total amounts of physical gold and silver held in all known depositories, ETFs and mutual funds as of the close of business on Friday.

During the week just past, there were a net 3.430 million troy ounces of gold added...with the lion's share of that increase being COMEX related once again -- but only a net 533,000 troy ounces of silver were added...and that number is only tiny because of the huge withdrawals from SLV this past week that have masked the big deposits into the COMEX. Click to enlarge.

According to Nick Laird's data on his website, a net 12.915 million troy ounces of gold were added to all the world's known depositories, mutual funds and ETFs during the last four weeks -- with virtually all of it going into either the COMEX or GLD...mostly the former. And a net 22.282 million troy ounces of silver were were also added during that same time period. That number would be 36 million ounces larger if it hadn't been for the big withdrawals from SLV during that time period.

Retail bullion sales, from what I've heard from my sources, is barely OK. Premiums remain at rock bottom -- and I haven't seen any sign that they've been raising them at all. There are some really great deals to be had out there. It remains a buyer's market for physical at the retail level, but for a limited time only I'm sure...judging by what's happening in the good delivery bar market.

At some point there will be large quantities of silver required by all the ETFs and mutual funds once serious institutional buying really kicks in -- and there were certainly signs of that, both this week and last. But the really big buying lies ahead of us when the silver price is finally allowed to rise substantially, which I'm sure is something that the powers-that-be in the silver world are keenly aware of -- and why they're desperate in their attempts to keep it from rising any faster than it already is. Their efforts were on full display once again yesterday -- and all this past week...but can't last forever.

And as Ted stated a while ago now, it would appear that JPMorgan has parted with most of the at least one billion troy ounces that they'd accumulated since the drive-by shooting that commenced at the Globex open at 6:00 p.m. EDT on Sunday, April 30, 2011.

They had to supply huge amounts to both India and China in 2024 -- and one has to suspect that this amount of demand will continue in 2025 as well...if not increase further. I suspect that all the silver flown into the COMEX from London so far this month, came from their stash.

The physical demand in silver at the wholesale level continues unabated -- and was beyond ginormous again this past week. The amount of silver being physically moved, withdrawn, or changing ownership continued without letup. That was on prominent display during the December delivery month, as 40.435 million troy ounces of physical silver were delivered/changed hands -- and the 11.85 million troy ounces of silver in January. So far in February, there have been a further 16.64 million troy ounces issued and stopped.

New silver has to be brought in from other sources [JPMorgan in London] to meet the ongoing demand for physical metal...as all the metal in New York is already spoken for and not for sale. That's been more than obvious on the COMEX in the past few weeks...while the withdrawals from SLV continue almost unabated. This demand will continue until available supplies are depleted...which will most likely be the moment that JPMorgan & Friends stop providing silver to feed this deepening structural deficit, now in its fifth year.

The vast majority of precious metals being held in these depositories are by those who won't be selling until the silver price is many multiples of what it is today.

Sprott's PSLV is the third largest depository of silver on Planet Earth with 180.6 million troy ounces...unchanged for the last six weeks -- and now an even greater distance behind the COMEX, where there are 363.4 million troy ounces being held...up another 16.6 million troy ounces this past week...but minus the 103 million troy ounces being held in trust for SLV by JPMorgan.

That 103 million ounce amount brings JPMorgan's actual silver warehouse stocks down to around the 46 million troy ounce mark...quite a bit different than the 148.6 million they indicate they have...up another 3.7 million ounces on the week.

But PSLV is a long way behind SLV, as they are the largest silver depository, with 430.5 million troy ounces as of Friday's close...down another 15.8 million troy ounces on the week.

The latest short report from last Monday [for positions held at the close of business on Wednesday, January 15] showed that the short position in SLV dropped by a meaningless 2.14% from the 47.09 million shares sold short in the prior report...down to a still eye-watering 46.08 million shares in this latest report. This remains grotesque beyond description.

BlackRock issued a warning several years ago to all those short SLV, that there might come a time when there wouldn't be enough metal for them to cover. That would only be true if JPMorgan decides not to supply it to whatever entity requires it...which is most certainly a U.S. bullion bank, or perhaps more than one.

The next short report...for positions held at the close of trading on Friday, January 31...will be posted on The Wall Street Journal's website this coming Tuesday evening, February 11.

Then there's that other little matter of the 1-billion ounce short position in silver held by Bank of America in the OTC market...with JPMorgan & Friends on the long side. Ted said it hadn't gone away -- and he'd also come to the conclusion that they're short around 25 million ounces of gold with these same parties as well.

The latest report for the end of Q3/2024 from the OCC came out about six weeks ago now -- and after careful scrutiny, I noted that the dollar value of their derivative positions were up just under 20 percent on average over the last quarter...the same percentage increase as Q2/2024. I suspect that it was entirely due to the price increases in both gold and silver since the Q2 report came out.

This OCC indicator is flawed for two very important reason, as way back 10-15 years ago, this report used to include the top dozen or so U.S. banks -- and included the likes of Wells Fargo and Morgan Stanley, amongst others...that are card-carrying members of the Big 8 shorts. Now the list is down to just four banks...so a lot of data is hidden...which is certainly the reason that the list was shortened. On top of that, the list doesn't include the non-U.S. banks that are members of the Big 8 shorts: British, French, German and Canadian banks.

-------

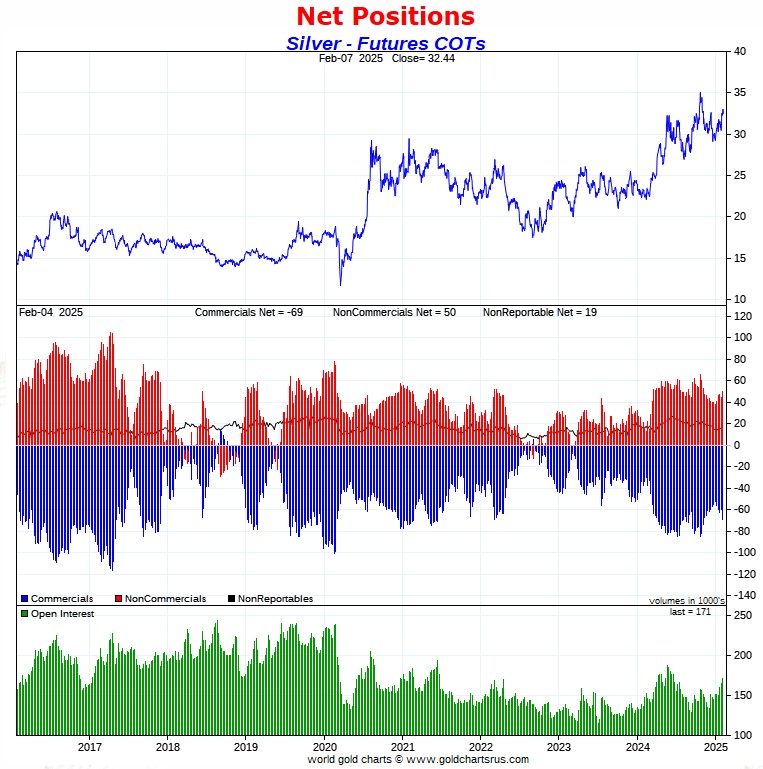

The Commitment of Traders Report, for positions held at the close of COMEX trading on Tuesday, showed increases in the commercial net short positions in both gold and silver -- and it was far worse than I was expecting in the latter.

In silver, the Commercial net short position increased by a very hefty 8,739 COMEX contracts, or 43.695 million troy ounces of the stuff...but a lot of that was Ted's raptors selling long positions, which had the mathematical effect of increasing the long position. But it was in the Big 4/8 category where things were ugly -- and I'll get into that in a bit.

The increase in the Commercial net short position in silver came about through the sale of 6,840 long contracts -- and 1,899 short contracts were sold as well. It's the sum of those two numbers that represents their change for the reporting week.

Under the hood in the Disaggregated COT Report, it was all Managed Money traders, plus more...as they increased their net long position by 10,297 COMEX contracts...which they accomplished through the purchase of 9,730 long contracts -- and also bought back 567 short contracts. It's the sum of those two numbers that represents their change for the reporting week.

The traders in the Nonreportable/small traders category also increased their net long position...them by 2,746 COMEX contracts...which meant that to balance things out, the traders in the Other Reportables category decreased their long position by 4,304 contracts.

Doing the math: 10,297 plus 2,746 minus 4,304 equals 8,739 COMEX contracts...the change in the commercial net short position.

The traders in the 'Other Reportables' category mentioned above, bought 3,038 short contracts during the reporting week -- and if it was one trader that put on that position, there's now a very slim chance that they are in the Big 8 commercial category...but I'm betting they aren't.

The Commercial net short positionin silver now stands at 69,007 COMEX contracts/345.035 million troy ounces...up those 8,739 contracts from the 60,268 contracts/301.340 million troy ounces they were short in last Friday's COT Report.

The Big 4 shorts [most likely the Big 1 or 2] increased their net short position by a hefty 2,105 COMEX contracts...from 57,136 contracts, up to 59,241 contracts...and the largest short position they've held for as long as I've had records -- and beyond monstrously bearish.

The Big '5 through 8' shorts also increased their net short position, them by 915 COMEX contracts...from the 21,963 contracts in the prior COT Report, up to 22,878 contracts in yesterday's COT Report -- and a tad under a record short position for them.

The Big 8 shorts in total increased their overall net short position from 79,099 contracts, up to 82,119 COMEX contracts week-over-week...an increase of 3,020 COMEX contracts...which is a lot. This is the largest Big 8 short position since July 16 of last year.

But since the Commercial net short position increased by 8,739 contracts in yesterday's COT Report -- and the Big 8 increased their short position by only 3,020 contracts, this meant that Ted's raptors...the small commercial traders other than the Big 8...had to have been huge sellers during the reporting week as well -- and they were...decreasing their long position by 8,739-3,020=5,719 COMEX contracts.

That decreased the raptor's long position from 18,831 COMEX contracts, down to 13,112 contracts. In the October 25, 2024 COT Report, they were net short silver by 7,356 COMEX contracts.

Here's Nick's 9-year COT chart for silver -- and updated with the above data. Click to enlarge.

If you're looking for a reason why the silver price action was so punk during the last reporting week, you don't need to look any further than this report ...as the collusive commercial traders of whatever stripe combined to sell just under 44 million ounces of paper silver.

The Big 4 short position...which in reality is mostly down to the Big 1 or 2...is, as I stated earlier, at an all-time record high -- and the Big 8 short position in total is only a hair below its record high of 83,091 contracts that they held back in the July 9, 2024 COT Report.

The Big 8 collusive commercial traders are now net short 48.1 percent of the total open interest in silver in this week's COT Report, compared to the 47.9 percent they were net short in the last COT Report.

That number in silver would have been a bit higher if it had not been for the 5,591 contract increase in total silver open interest...which obviously affects the percentage calculation.

However, no matter how you slice it or dice it, from a COMEX futures market perspective, the set-up remains off-the-charts bearish in the extreme.

As I've been saying recently, I've come to the conclusion that the Big 8 collusive commercial shorts have no intention of ever covering any or all of their short positions -- and it's now strictly a price management tool to prevent a silver price explosion. It's always been that way, of course...but is now institutionalized -- and it's for that reason I've lost most of my fear of it...especially considering demand for immediate delivery in the physical market.

However, nothing has changed with regards to that ongoing and deepening structural deficit in the physical market...which is now in its fifth consecutive year.

It's more than obvious from the price action that silver wants to rise sharply to reflect that...like it's been doing all week -- and again on Friday. But it's not being allowed at the moment, as the paper hangers in the COMEX futures market in New York have been working overtime to ensure that it doesn't.

As it's been for decades, it only matters what the collusive Big 8 commercial traders do...especially the Big 1 or 2...both of which are bullion banks, I'm sure. Right now they're sitting there like a lump...the cork in the silver price bottle as short sellers of last resort...which they were again this week -- and in spades.

-------

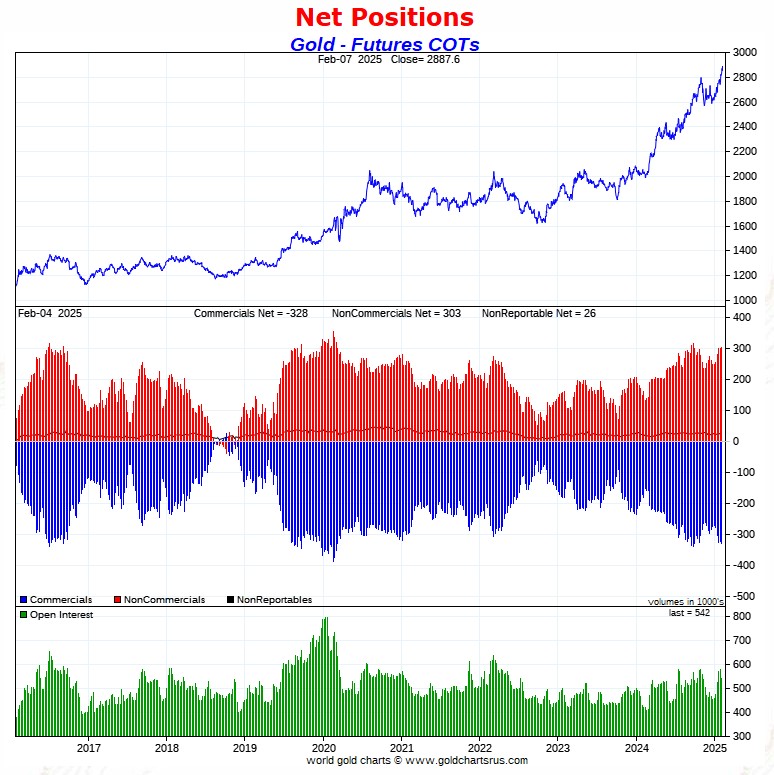

In gold, the commercial net short position increased by only 4,453 contracts, or 445,300 troy ounces of the stuff.

They arrived at that number under the strangest of circumstances...decreasing their long position by 35,656 contracts -- and also decreasing their short position by 31,203 COMEX contracts. It's the difference between those two numbers that represents their change for the reporting week.

Under the hood in the Disaggregated COT Report the Managed Money traders didn't do much in the overall...actually decreasing their net long position by 1,007 contracts...which they arrived at through the purchase of 12,614 long contracts, along with the sale of 13,621 short contracts. It's the difference between those two numbers that represents their change for the reporting week.

The traders in the Other Reportables and Nonreportable/small traders increased their net long positions...the former by 4,106 COMEX contracts -- and the latter by 1,354 contracts.

Doing the math: 4,106 plus 1,354 minus 1,007 equals 4,453 COMEX contracts, the change in the commercial net short position.

The commercial net short position in gold now sits at 328,175 COMEX contracts/32.818 million troy ounces of the stuff...up those 4,453 contracts from the 323,722 contracts/32.372 million troy ounces they were short in last Friday's COT Report -- and obviously beyond wildly bearish.

The Big 4 shorts in gold decreased their net short position for the second week in a row, them by a very decent 9,770 contracts...from 185,379 contracts they were short in the last COT report, down to 175,609 contracts in yesterday's report -- but still über bearish.

However, the Big '5 through 8' shorts increased their net short position for the fifth week in a row, this time by a whopping 11,058 contracts...from the 66,990 contracts they were short in last Friday's COT Report, up to 78,048 contracts held short in the current COT Report...which is on the bearish side for them...but not a record short position.

The Big 8 short position in total only increased by a small amount... from 252,369 COMEX contracts/25.237 million troy ounces in last Friday's COT Report...up to 253,657 contracts/25.366 million troy ounces in yesterday's... an increase of only 1,288 COMEX contracts.

But since the commercial net short position increased by 4,453 COMEX contracts during the reporting week -- and the Big 8 commercial short position increased by only 1,288 COMEX contracts, that meant that Ted's raptors... the small commercial traders other than the Big 8 had to have been sellers during the reporting week just past as well -- and they were...for the fourth week in a row. They increased their grotesque short position by a further 4,453-1,288=3,165 COMEX contracts. Their short position is now 74,518 contracts...up from the 71,353 contracts they were short in last Friday's COT Report. This is another new record high short position for them.

Words, as I say in this spot every week, continue to fail me on this issue...as I cannot overemphasize just how grotesque and obscene the raptor short position in gold is on an historical basis -- and despite this huge short position, it's a near mathematical impossibility that there's a Managed Money or Other Reportables trader in the Big '5 through 8' category in gold. This appears to be a strictly uncontaminated commercial short position.

Here's Nick's 9-year COT chart for gold -- and updated with the above data. Click to enlarge.

Once again, this tiny change in the commercial net short position in gold in yesterday's COT Report barely moved the needle on its grotesque commercial net short position...but in the wrong direction compared to last week.

At some point these short positions have to be covered...especially those raptors -- and will only happen on fantastically lower prices which, as I said last week and the week before, ain't going to happen...not now, or ever. That's why closing the COMEX -- and maybe the LBMA as well, remains the only options to save the shorts from Ted's 'Bonfire'...unless the powers-that-be have another treachery up their sleeves. I have more on this in The Wrap.

The Big 8 collusive commercial traders are short 46.8 percent of total open interest in the COMEX futures market...up from the 43.7 percent they were short in the prior COT Report. Part of the reason for that increase, was because of the 35,501 contract decrease in total open interest, which obviously affects the calculation.

But once you add in the 74,518 contracts currently held short by Ted's raptors, the commercial net short position in gold works out to 60.5 percent of total open interest, up big from the 56.1 percent they were short in the prior COT Report...which is grotesque and obscene beyond description.

That percentage number was up big this week because of that 35,501 contract drop in total open interest.

Can gold rally big from here? Of course...as can silver...as we've witnessed this week -- and up until mid-morning COMEX trading in New York on Friday. But that only happened because the big commercial shorts allowed it -- and they didn't hesitate to step in with a vengeance when both were apparently going to run away to the upside.

But this eye-opening dichotomy between the huge raptor long position in silver...13,112 contracts vs. the monster short position held by the raptors in gold...74,518 contracts...remains unprecedented. For the most part, these small traders are all the same players in both these precious metals -- and what that means for their respective prices going forward, is anyone's guess.

To sum up, from a COMEX futures market perspective, the set-up in gold remains off-the-charts bearish. But, as said about silver...at some point, as Ted mentioned repeatedly over the years, what the numbers in the COT Report show, won't matter, as they will be trumped by factors beyond the control of the paper hangers in New York.

That process may be in progress now, but it's not being allowed to manifest itself in the prices of either silver or gold at the moment...as the commercial traders of whatever stripe continue to step in as not-for-profit sellers when required.

------

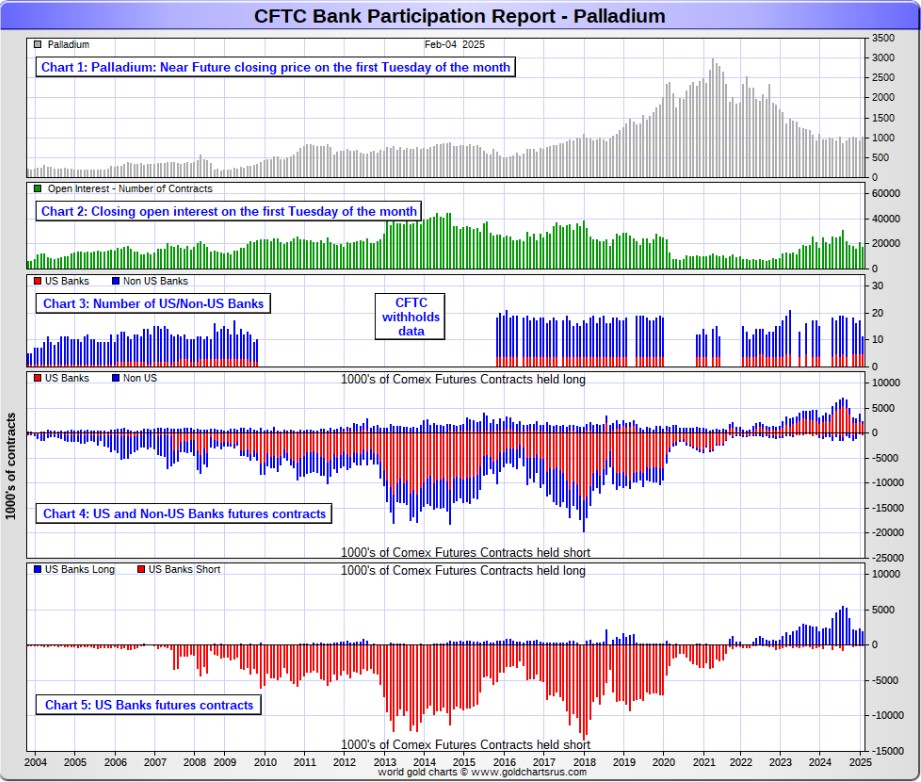

In the other metals, the Managed Money traders in palladium reduced their net short position by a further and hefty 1,673 COMEX contracts -- but remain net short palladium by 6,905 contracts...40.2 percent of total open interest. The commercial traders in the Producer/ Merchant category are now back on the short side by a bit for the second week in a row, while the other three categories of traders are all net long palladium...especially the Swap Dealers in the commercial category.

In platinum, the Managed Money traders increased their net long position by a further and chunky 8,975 COMEX contracts during the reporting week -- and are now net long platinum by 11,485 COMEX contracts.

The commercial traders in the Producer/Merchant category in platinum are meganet short a knee-wobbling 24,076 COMEX contracts -- but the Swap Dealers in the commercial category are net long platinum, but now only a tiny 337 contracts. The traders in both the Other Reportables and Nonreportable/ small traders categories remain net long platinum by very hefty amounts... especially the Other Reportables.

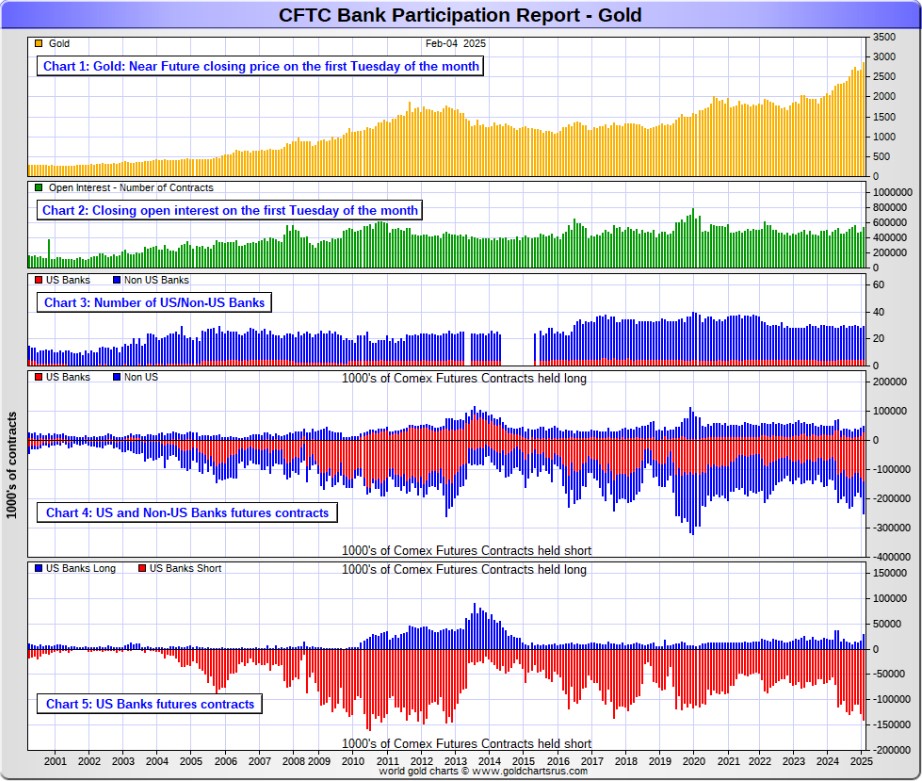

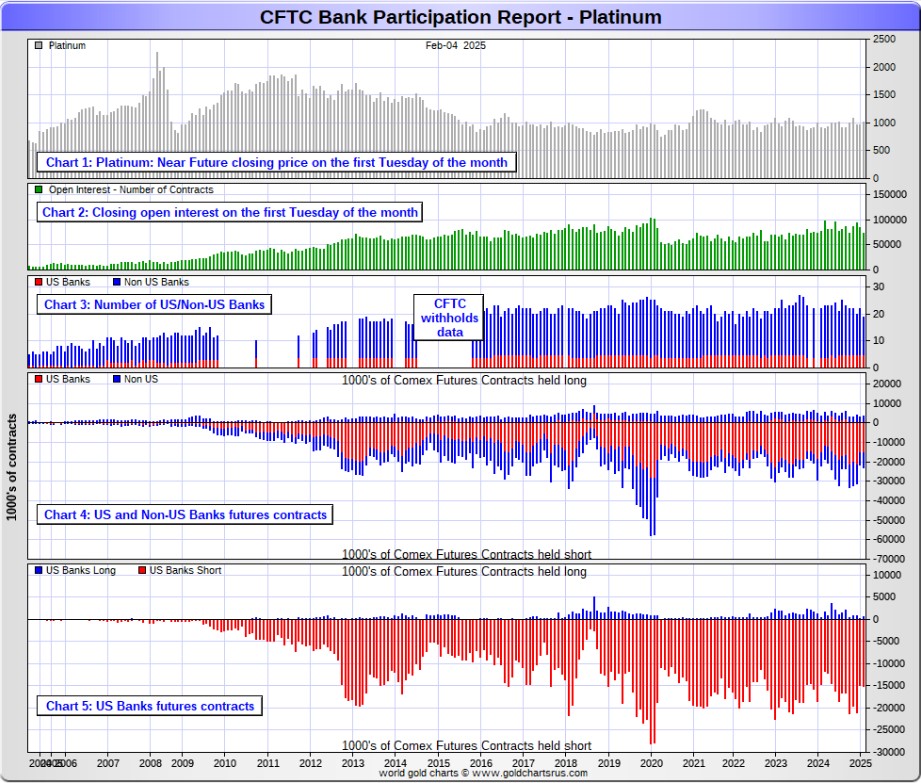

It's mostly the world's banks in the Producer/Merchant category that are 'The Big Shorts' in platinum in the COMEX futures market, as per February's Bank Participation Report that came out yesterday -- and have increased their short position in platinum by a bit since the January report.

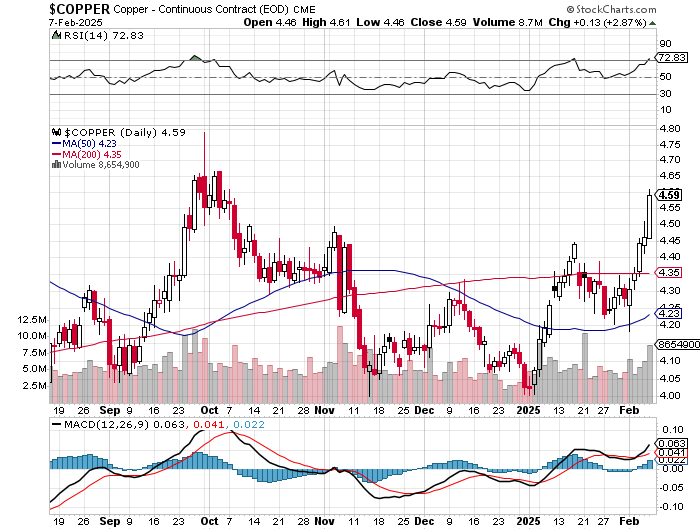

In copper, the Managed Money traders increased their net long position by 1,922 contracts -- and are net long copper by 18,464 COMEX contracts...about 461 million pounds of the stuff as of yesterday's COT Report...up from the 413 million pounds they were net long copper in last Friday's COT report.

Copper, like platinum, continues to be a wildly bifurcated market in the commercial category. The Producer/Merchant category is net short 39,200 copper contracts/980 million pounds -- while the Swap Dealers are net long 20,490 COMEX contracts/512 million pounds of the stuff.

Whether this means anything or not, will only be known in the fullness of time. Ted said it didn't mean anything as far as he was concerned, as they're all commercial traders in the commercial category. However, this bifurcation has been in place for as many years as I can remember -- and that's a lot.

In this vital industrial commodity, the world's banks...both U.S. and foreign...are net long 6.9 percent of the total open interest in copper in the COMEX futures market as shown in the February Bank Participation Report that came out yesterday -- and down from the 8.4 percent they were net long in January's.

At the moment it's the commodity trading houses such as Glencore and Trafigura et al., along with some hedge funds, that are net short copper in the Producer/Merchant category, as the Swap Dealers are net long, as pointed out above.

The next Bank Participation Report is due out next Friday, March 7.

------

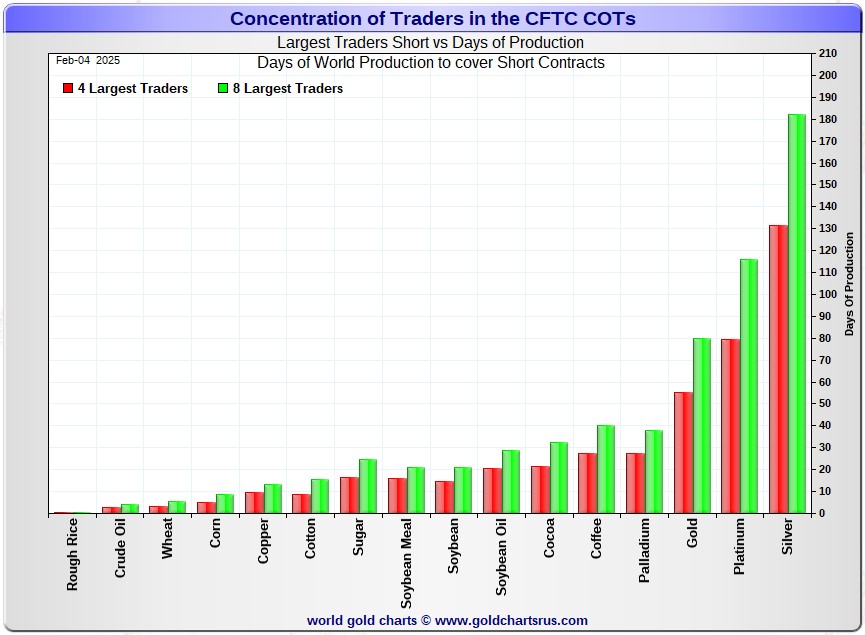

Here’s Nick Laird’s “Days to Cover” chart, updated with the COT data for positions held at the close of COMEX trading on Tuesday, February 4. It shows the days of world production that it would take to cover the short positions of the Big 4 — and Big '5 through 8' traders in every physically traded commodity on the COMEX. Click to enlarge.

In this week's data, the Big 4 traders are short 131 days of world silver production...up about four days from the prior COT report. The ‘5 through 8’ large traders are short an additional 51 days of world silver production...up two days from the last COT Report, for a total of about 182 days that the Big 8 are short -- and obviously up six days from last Friday's COT report.

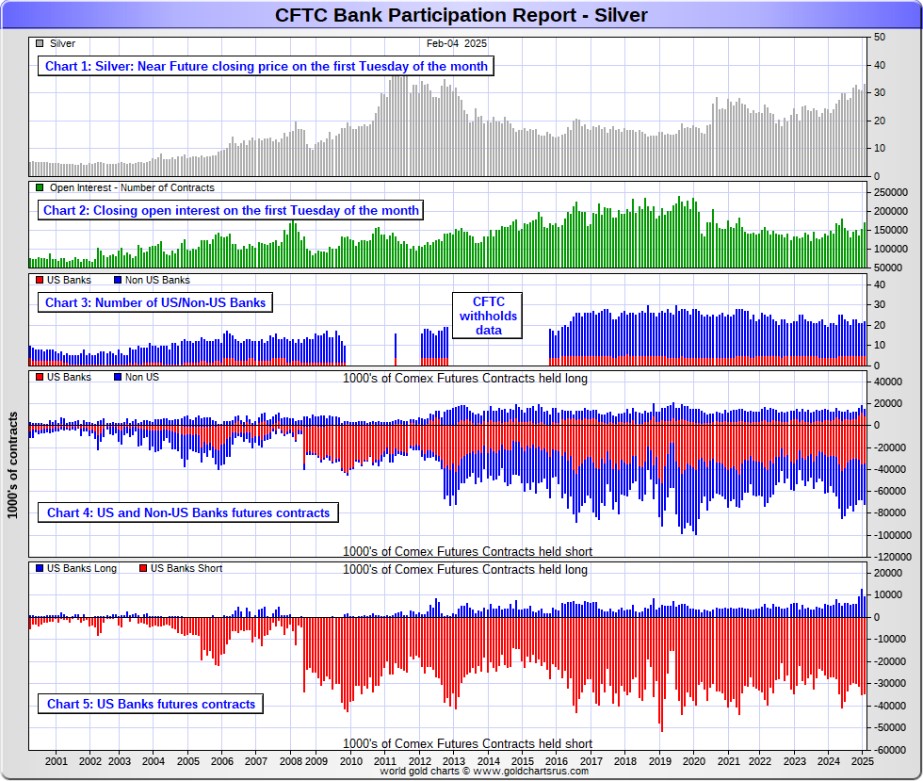

Those 182 days that the Big 8 traders are short, represents a bit over 6 months of world silver production, or 410.595 million troy ounces/82,119 COMEX contracts of paper silver held short by these eight commercial traders. Several of the largest of these are now non-banking entities, as per Ted's discovery a year or so ago. February's Bank Participation Report continued to confirm that this is still the case -- and not just in silver, either.

As mentioned further up, the small commercial traders other than the Big 8 shorts, Ted's raptors, are net long silver by 13,112 COMEX contracts...down from the 18,831 contracts they were net long in last Friday's COT Report.

In gold, the Big 4 are short about 55 days of world gold production...down about 3 days from the prior COT Report. The Big '5 through 8' are short an additional 25 days of world production, up about 4 days from last the last report...for a total of 80 days of world gold production held short by the Big 8 -- and down about 1 day from last Friday's COT Report.

The Big 8 commercial traders are net short 48.1 percent of the entire open interest in silver in the COMEX futures market as of yesterday's COT Report, up a bit from the 47.9 percent they were net short in last Friday's report. It would have been up more than that if total open interest hadn't increased by 5,591 contracts during the reporting week...which obviously affects the percentage calculation.

In gold, it's 46.8 percent of the total COMEX open interest that the Big 8 are net short, up from the 43.7 percent they were net short in the last COT Report -- and up because of the 35,501 contract decrease in total open interest during the reporting week, which obviously affects the calculation in it as well.

But the total commercial net short position in gold is 60.5 percent of total open interest once you add in what Ted's raptors [the small commercial traders other than the Big 8] are short on top of that...a further 74,518 COMEX contracts.

Ted was of the opinion that Bank of America is short about one billion ounces of silver in the OTC market, courtesy of JPMorgan & Friends. He was also of the opinion that they're short 25 million ounces of gold as well. And the latest report from late December [for Q3/2024] shows that their positions are up 20 percent from what they were holding at the end of Q2/2024...with most of that increase most likely being price related. One wonders if Mr. Buffet is done dumping the rest of the stock he has in that company.

The short position in SLV now sits at 46.08 million shares as of the last short report, for positions held at the close of COMEX trading on Wednesday, January 15...down a tiny 2.14 percent from the 47.09 million shares sold short on the NYSE in the prior report. This, as you already know, is off-the-charts grotesque -- but yet another way that 'da boyz' are controlling the silver price.

The next short report is due out on Tuesday, February 11...for positions held at the close of COMEX trading on Friday, January 31.

The situation regarding the Big 4/8 commercial short positions in the COMEX futures market in both silver and gold remains beyond wildly bearish in both -- and is now a strictly price controlling mechanism.

As Ted had been pointing out ad nauseam, the resolution of the Big 4/8 short positions will be the sole determinant of precious metal prices going forward -- although the record high short position held by Ted's raptors in gold continues to be a Sword of Damocles in its own right.

------

The February Bank Participation Report [BPR] data is extracted directly from yesterday's Commitment of Traders Report data. It shows the number of futures contracts, both long and short, that are held by all the U.S. and non-U.S. banks as of last Tuesday’s cut-off in all COMEX-traded products.

For this one day a month we get to see what the world’s banks have been up to in the precious metals. They’re usually up to quite a bit -- and they certainly were again this past month.

[The February Bank Participation Report covers the four-week time period from January 7 to February 4 inclusive]

In gold, 5 U.S. banks are net short 110,135 COMEX contracts, down a paltry 1,012 contracts from the 111,147 contracts that these same 5 U.S. banks were net short in January's BPR. These U.S banks have been mega net short gold since July of last year.

Also in gold, 24 non-U.S. banks are net short 91,576 COMEX contracts, up a whopping 50,178 contracts from the 41,938 contracts that 23 non-U.S. banks were short in January's BPR...the highest they've been since the March 2022 BPR.

At the low back in the August 2018 BPR...these non-U.S. banks held a net short position in gold of only 1,960 contacts -- so they've been back on the short side in an enormous way ever since. Only a tiny handful of these banks hold a meaningful short position in gold. The short positions of the rest are of no consequence -- and never have been. A few of them may actually be net long gold by a bit.

Although some of the largest U.S. and foreign bullion banks are in the Big 8 short category in gold, some of the hedge fund/commodity trading houses are short even more grotesque amounts of gold than the banks in the Big 4/8 category.

It's also a strong possibility that the BIS could be short gold in the COMEX futures market as well.

As of February's Bank Participation Report, 29 banks [both U.S. and foreign] were net short 37.2 percent of the entire open interest in gold in the COMEX futures market...up a whole bunch from the 31.9 percent that 28 banks were net short in the January BPR.

Here’s Nick’s BPR chart for gold going back to 2000. Charts #4 and #5 are the key ones here. Note the blow-out in the short positions of the non-U.S. banks [the blue bars in chart #4] when Scotiabank’s COMEX short position was outed by the CFTC in October of 2012. Click to enlarge.

In silver, 5 U.S. banks are net short 25,160 COMEX contracts, up 3,117 contracts from the 22,043 contracts that these same 5 U.S. banks were short in the January BPR. This is the larges short position they've held since the August 2024 BPR.

The biggest short holders in silver of the five U.S. banks in total, would be Citigroup, Wells Fargo, Bank of America -- and maybe JPMorgan from time to time.

Also in silver, 17 non-U.S. banks are net short 31,737 COMEX contracts, up a hefty 5,072 contracts from the 26,665 contracts that that 16 non-U.S. banks were short in the January BPR...their biggest short position since last November's BPR.

It's a given that HSBC, Barclays and Standard Chartered hold by far the lion's share of the short position of these non-U.S. banks...as do some of Canada's banks as well...with the Bank of Montreal and Scotia Capital/Scotiabank coming to mind.

And, like in gold, the BIS could also be actively shorting silver. The remaining short positions divided up between the other 12 or so non-U.S. banks are immaterial — and have always been so....the same as most of the 24 non-U.S. banks in gold as well.

As of February's Bank Participation Report, 22 banks [both U.S. and foreign] were net short 33.4 percent of the entire open interest in silver in the COMEX futures market...which remains outrageous — and up from the 32.1 percent that 21 banks were net short in the January BPR.

Here’s the BPR chart for silver. Note in Chart #4 the blow-out in the non-U.S. bank short position [blue bars] in October of 2012 when Scotiabank was brought in from the cold. Also note August 2008 when JPMorgan took over the silver short position of Bear Stearns—the red bars. It’s very noticeable in Chart #4—and really stands out like the proverbial sore thumb it is in chart #5. Click to enlarge.

In platinum, 5 U.S. banks are net short 14,306 COMEX contracts in the February BPR, down a tiny 247 contracts from the 14,553 contracts that these same 5 U.S. banks were short in the January BPR -- but still an horrific amount.

At the 'low' back in September of 2018, these U.S. banks were actually net long the platinum market by 2,573 contracts. So they have a very long way to go just to get back to market neutral in platinum...if they ever intend to, that is. They look permanently stuck on the short side to me, a fact that I point out from time to time.

Also in platinum, the non-U.S. banks increased their net short position by 1,063 contracts...from 4,386 contracts held by 17 banks in January's BPR... up to 5,449 contracts that only 14 non-U.S. banks were net short in the February BPR.

Back in the December 2023 BPR, these non-U.S. banks were net short a microscopic 35 platinum contracts...so they've got more work to do if they ever want to get back to that number.

As you already know, platinum remains the big commercial shorts No. 2 problem child after silver. How it will ultimately be resolved is unknown, but most likely in a paper short squeeze, as the known stocks of platinum are minuscule compared to the size of the short positions held -- and that's just the short positions of the world's banks I'm talking about here.

Of course there's now a long-term structural deficit in it [and palladium] as well -- and I had a story about that in Friday's column.

And as of February's Bank Participation Report, 19 banks [both U.S. and foreign] were net short 27.0 percent of platinum's total open interest in the COMEX futures market, up from the 22.4 percent that 22 banks were net short in January's BPR.

Here's the Bank Participation Report chart for platinum. Click to enlarge.

In palladium, 5 U.S. banks are net long 1,764 COMEX contracts in the February BPR, down 382 contracts from the 2,146 contracts that that these same 5 U.S. banks were net long in the January BPR.

Also in palladium, now only 6 non-U.S. banks are net long 240 COMEX contracts, down from the 1,438 contracts that 12 non-U.S. banks were net long in the January BPR.

And as I've been commenting on for almost forever, the COMEX futures market in palladium is a market in name only, because it's so illiquid and thinly-traded. Its total open interest in yesterday's COT Report was only 17,168 contracts...compared to 73,237 contracts of total open interest in platinum...170,726 contracts in silver -- and 542,004 COMEX contracts in gold.

Total open interest in palladium has increased quite a bit over the last few years, because I remember when it was less than 9,000 contracts. So it's nowhere near as illiquid as it used to be -- and it's also been helped along by the fact that the bid/ask is now only 40 bucks. It used to be $150 at one point way back when.

As I say in this spot every month, the only reason that there's a futures market at all in palladium, is so that the Big 8 commercial traders can control its price. That's all there is, there ain't no more.

As of this Bank Participation Report, now only 11 banks [both U.S. and foreign] are net long 11.6 percent of total open interest in palladium in the COMEX futures market...down from the 16.9 percent of total open interest that 17 banks were net long in the January BPR.

For the last 5 years or so, the world's banks have not been involved in the palladium market in a material way...see its chart below. And with them still net long, it's almost all hedge funds and commodity trading houses that are left on the short side. The Big 8 commercial shorts, none of which are banks, are short 40.5 percent of total open interest in palladium as of yesterday's COT...down about 15 percentage points month-over-month.

Here’s the palladium BPR chart. Although the world's banks are net long at the moment, it remains to be seen if they return as big short sellers again at some point like they've done in the past. Click to enlarge.

Excluding palladium for obvious reasons, and almost all of the non-U.S. banks in gold, silver and platinum...only a small handful of the world's banks, most likely no more than 5 or so in total -- and mostly U.S. and U.K.-based...along with [maybe] the BIS...continue to hold meaningful short positions in the other three precious metals...although I won't let Canada's Bank of Montreal or Scotia Capital/Scotiabank off the hook just yet.

As I pointed out above, some of the world's commodity trading houses and hedge funds are also mega net short the four precious metals...far more short than the U.S. banks in some cases. They have the ability to affect prices if they choose to exercise it...which I'm sure they're doing at times -- and this is particularly obvious in the thinly-traded and illiquid palladium market. But it's still the collusive Anglo/American banking cartel in the commercial category that are at Ground Zero of the price management scheme in the COMEX futures market in the other three.

And as has been the case for years now, the short positions held by the Big 4/8 traders is the only thing that matters...especially the short positions of the Big 4...or maybe only the Big 1 or 2 in both silver and gold. How this is ultimately resolved [as Ted kept pointing out] will be the sole determinant of precious metal prices going forward.

The Big 8 commercial traders continue to have an iron grip on their respective prices, which was on full display every day this past week -- and it will remain that way until they either relinquish control voluntarily, are told to step aside...or get overrun.

Considering the current state of affairs of the world as they stand today -- and the structural deficit in silver -- and now in platinum and palladium as well, the chance that these big bullion banks and commodity trading houses could get overrun at some point, is no longer zero -- and certainly within the realm of possibility if things go totally non-linear, as they just might if the drain on LBMA gold and silver stockpiles continues.

But...as Ted kept reminding us from time to time...if they do finally get overrun, it will be for the very first time...which obviously wasn't allowed to happen this past month, either.

The next Bank Participation Report is due out on Friday, March 7.

I have an average number of stories, articles and videos for you today.

-----

CRITICAL READS

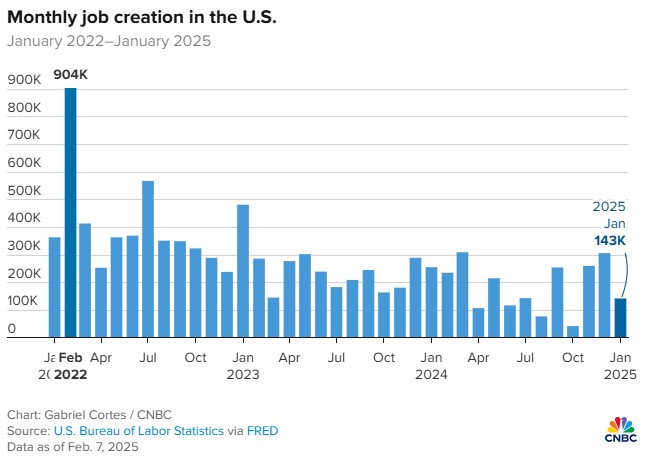

U.S. economy added just 143,000 jobs in January, but unemployment rate fell to 4%

Job creation was lower than expected in January, though the unemployment rate edged down and worker wages rose sharply, the Bureau of Labor Statistics reported Friday.

Non-farm payrolls climbed by a seasonally adjusted 143,000 for the month, down from an upwardly revised 307,000 in December and below the 169,000 forecast from Dow Jones. The unemployment rate nudged lower to 4%.

The report also featured significant benchmark revisions to the 2024 totals that saw substantial downward changes to the previous payrolls level though upward revisions to those who reported holding jobs. Click to enlarge.

The revisions, which the BLS does each year, reduced the jobs count by 589,000 in the 12 months through March 2024. A preliminary adjustment back in August 2024 had indicated 818,000 fewer jobs.

This news item showed up on the cnbc.com Interne site at 8:31 a.m. on Friday morning EST -- and I thank Swedish reader Patrik Ekdahl for today's first story. Another link to it is here. The Zero Hedge spin on this is headlined "January Jobs Growth Below Estimates Amid Massive Revisions Which Trim Unemployment, Reduce Historic Payrolls" -- and linked here.

------

Consumer Credit Unexpectedly Surges By Most on Record Despite All-Time High APRs

We have repeatedly warned that with their savings - and especially "emergency covid savings" - gone or nearly gone, Biden admin savings data manipulation notwithstanding...

... U.S. consumers had no choice but to max out their credit cards in order to "extend and pretend" their moment of purchasing greatness, or as we called it two months ago, their last hurrah, a hurrah that would last very briefly as it was only a matter of months if not weeks before said cards were denied.

One month later, that's exactly what happened, when to our surprise, revolving credit cratered at the fastest pace since the covid crash, contracting a whopping $7.5 billion, an event which for a country that lives on debt -- literally - is unheard of outside of a recession.

And while it would have been normal, if not expected, for credit card balances to continue declining with savings rates near record lows and with credit card rates at record highs, trust the U.S. economy to do precisely the opposite of what is logical and according to the latest just released consumer credit data, U.S. consumers exited 2024 with a bang after Consumer credit soared by a record $40.8 billion in December, a complete reversal of the $5.4 billion November drop, and a month that sticks out like a sore thumb in the history of consumer credit as shown below.

The December print is all the more remarkable when considering that Wall Street consensus was for a $14.6BN consumer credit print. This means that the actual number was a 4 sigma beat to expectations, the biggest on record for this particular data series.

This multi-chart Zero Hedge news item was posted on their Internet site at 3:46 p.m. on Friday afternoon EST -- and another link to it is here.

------

The Dog That Does More Than Bark -- Doug Noland

Treasury Secretary Scott Bessent’s Thursday comment is credible: “The President wants lower rates. He and I are focused on the 10-year Treasury and what is the yield of that.”

“Everyone has a plan, until they get punched in the mouth” (Mike Tyson). The Trump administration definitely has some grandiose plans. Dressed in baggy attire and too often projecting a pacifist temperament - but when pushed too far, the bond market can reveal the inner brute force of a prizefighter. Global bond markets have been agitated over recent months. The resurrected bond vigilantes have been circling.

But global bonds have enjoyed a nice rally of late. After trading at 4.80% on January 14th, 10-year Treasury yields touched a seven-week low 4.40% during Wednesday trading. UK gilt yields dropped from a 4.92% trading high to 4.37%; French yields 3.49% to 3.05%; German yields 2.65% to 2.34%; Italian yields 3.85% to 3.43%; Canadian yields 3.56% to 2.88%; and Australian yields 4.66% to 4.29%.

Sinking Treasury yields were especially pacifying for distressed EM bonds. Brazil’s dollar bond yields sank from 7.11% to 6.49%, with Mexico’s yields falling from 6.80% to 6.38%. Local currency yields swung from 10.46% to 9.71% in Mexico and from 15.44% to 14.31% in Brazil.

If I were the bond market, I’d be leery of a budget big on tax cuts offset by indeterminate revenue sources. This becomes a more pressing issue for a bond market facing heightened overheating risks.

I appreciate that the levered players maintain high confidence that the Fed will ensure Treasury market liquidity. It must be further comforting to have a seasoned hedge fund operator now in charge of the Department of Treasury – specifically underscoring the administration’s focus on Treasury yields.

But this is a unique environment with a unique medley of risks, including runaway deficit spending, economic overheating, inflation, trade wars, possible Fed tightening and erratic Washington and global policy making. It’s just difficult to believe that players are comfortable operating these days neck deep in speculative leverage. Some seem darn right uncomfortable. Gold surged to record highs, adding another $63 to end the week at $2,861.

This interesting commentary from Doug appeared on his Internet site around midnight Friday PST -- and another link to it is here. Gregory Mannarino's post market close rant for Friday is linked here -- and this one runs for 43 minutes.

-------

Three very worthwhile and informative interviews

1. Can the U.S. Own Gaza? -- Colonel Douglas Macgregor

This worthwhile 24-minute video interview with Colonel Macgregor was hosted by Judge Andrew Napolitano on Thursday -- and I thank Guido Tricot for sharing it with us. The link to it is here.

2. A War Criminal Visits the White House -- Phil Giraldi

This very interesting 24-minute video interview with former CIA intelligence offer Giraldi...with the Judge as host...was posted on the youtube.com Internet site on Thursday as well -- and I thank Guido for this one too. The link to it is here.

3. INTEL Roundtable with Larry Johnson & Ray McGovern -- Weekly Wrap

This 26-minute minute video interview with these two former CIA analysts appeared on the youtube.com Internet site later on Friday afternoon -- and is also hosted by Judge Napolitano. It also comes courtesy of Guido Tricot -- and the link to it is here.

------

Suddenly even the Financial Times can muse about gold revaluation

Another week, another record high for the gold price. Cue wild celebration among gold bugs -- and frantic speculation from everyone else about the reason for the explosion in demand for the precious metal.

Geopolitical turmoil is one obvious explanation. Inflation concerns amid insane tariff dramas is another. However, there is a third, less noticed, issue bubbling away too: some hedge fund contemporaries of Scott Bessent, the hedgie-turned-U.S. Treasury secretary, are speculating about a revaluation of America's gold stocks.

Currently these are valued at just $42 an ounce in national accounts. But knowledgeable observers reckon that if these were marked at current values -- $2,800 an ounce -- this could inject $800 billion into the Treasury General Account, via a repurchase agreement. That might reduce the need to issue quite so many Treasury bonds this year.

This week such chatter intensified after Bessent both pledged to "monetise the asset side of the U.S. balance sheet" -- in other words, to focus on assets as much as liabilities while also promising to lower 10-year Treasury yields.

"Re-marking ... to current market value would mechanically deleverage the U.S. balance sheet," says David Teeters of IESE business school, who notes that if gold prices keep rising, this potential blessing swells. Or as Larry McDonald, a libertarian analyst, notes: "It is time to get creative around ... Uncle Sam's balance sheet."

A decent amount of this interesting gold-related news item from the Financial Times on Friday is posted in the clear in this GATA dispatch -- and the rest is behind their paywall. Another link to it is here.

------

China starts pilot project allowing insurers to invest in gold

China, the world's biggest bullion consumer, will allow some of its insurance funds to buy gold for medium- and long-term asset allocations as part of a pilot project, the country's financial regulator said today.

The project should broaden institutional demand and may provide support to gold prices in China in the longer term depending on insurance funds' appetite for participating in it, according to analysts.

The 10 pilot participants include China Life Insurance, New China Life Insurance, and several subsidiaries of Ping An, the National Financial Regulatory Administration said in a notice.

"It will certainly be positive in terms of fresh demand. What we don't know is how much they would want, of course," said StoneX analyst Rhona OConnell.

The investment options under the programme include gold spot physical contracts, gold spot deferred delivery contracts, and gold leasing business listed or traded on the Shanghai Gold Exchange.

This Reuters story was picked up by the businesstimes.com.sg Internet site on Friday -- and the first person through the door with it was Roy Stephens -- and another link to it is here.

-------

China’s central bank maintains gold buying momentum in January

China's central bank added gold to its reserves in January for a third month, official data by the People’s Bank of China (PBOC) showed on Friday (February 7).

China’s gold reserves were 73.45 million fine troy ounces at the end of January, versus 73.29 million troy ounces a month earlier...an increase of 160,000 troy ounces.

The value of China’s gold reserves rose to US$206.53 billion at the end of last month from US$191.34 billion at the end of December.

Gold has reached an all-time high, breaking multiple records so far this year, largely due to the uncertainty surrounding U.S. President Donald Trump’s tariff policies, which have amplified concerns about global economic growth and inflationary pressures.

“I think it indicates that they feel that the trade war has got legs to run and that they’re concerned about how that might play out,” an independent metals analyst Ross Norman based in London said.

The U.S. imposed an additional 10 per cent tariff on Chinese imports that went into effect on Tuesday, and was met with a package of retaliatory measures from China.

This gold-related story appeared on the businesstimes.com.sg Internet site on Friday -- and I found it on Sharps Pixley. Another link to it is here.

------

MEME of the DAY

------

The WRAP

"Understand this. Things are now in motion that cannot be undone." -- Gandalf the White

------

Today's pop 'blast from the past' is 50 years young this year -- and both the American rock band that performs it -- and the song itself should be instantly recognizable. The link is here. Of course there's a bass cover to this -- and infusion26 lays it down just right. The link to that is here.

Today's classical 'blast from the past' is a continuation of J.S. Bach's Brandenburg's Concerto series. This week it's the No. 3 in G Major BWV 1048 -- and most likely the most well known, as the two movements have been used countless times as intros for TV and radio shows over the generations -- and should be familiar to most.

This performance is by the San Francisco-based 'Voices of Music' on original instruments -- and it's an audio/visual treat for both the ears -- and the eyes. The link is here.

------

The collusive commercial traders of whatever stripe were all over the precious metals like white on rice on Friday. In gold and silver, they capped their prices very shortly before that more-than-suspicious spike higher in the dollar index.

Gold traded above $2,900 in April -- and silver above $33 in March...their respective current front months -- but were both obviously hauled down and closed below both numbers -- and in the case of silver, well below it. Gold is a hair under the overbought mark on its RSI trace...but silver is closer to market neutral on its.

Although gold was allowed to close higher on the day, that luxury wasn't allowed in silver -- and I couldn't figure out why they were being so aggressive in silver until I received commentary from 'Alyosha' that Roy Stephens sent my way late yesterday afternoon.

His remarks were as follows..."There was an SLV option expiration today with about 3 million shares of $29 calls expiring. $32.22 = $28.95 SLV. COMEX March silver in hourly data below…Any questions?"

It's obvious that whatever member[s] of the Big 8 commercial shorts that wrote those calls, wanted them to expire worthless and collect the premium. Mission accomplished -- and the reason why the silver price got crushed on Friday.

Platinum traded in a $28 price range in its current front month, which is April -- and was closed down $12 bucks in the spot market...but only down $1.50 in April. Palladium was beaten up once again -- and at its intraday low tick, 'da boyz' had it below its 200-day moving average by a bit.

The managed money traders continue to pour onto the long side in copper, as its rally continued unabated yesterday. It was allowed to close higher by a further 13 cent at $4.59/pound -- and is now in overbought territory on its RSI trace by a bit. It's now only a matter of time before the collusive commercial shorts pull the pin on this rally and harvest all those newly-minted long contracts.

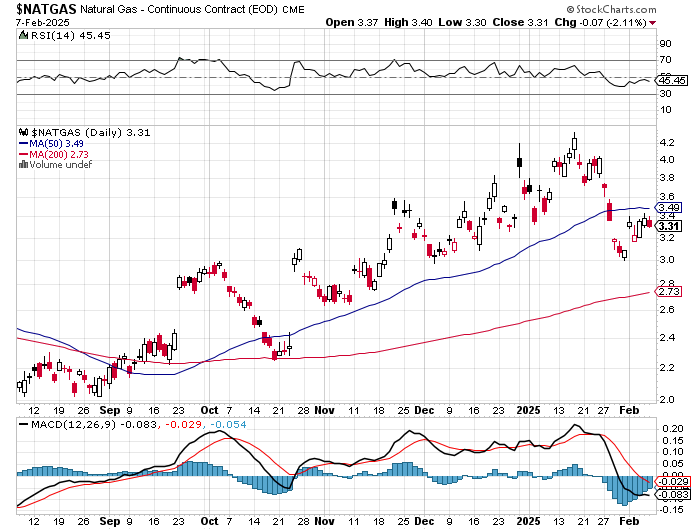

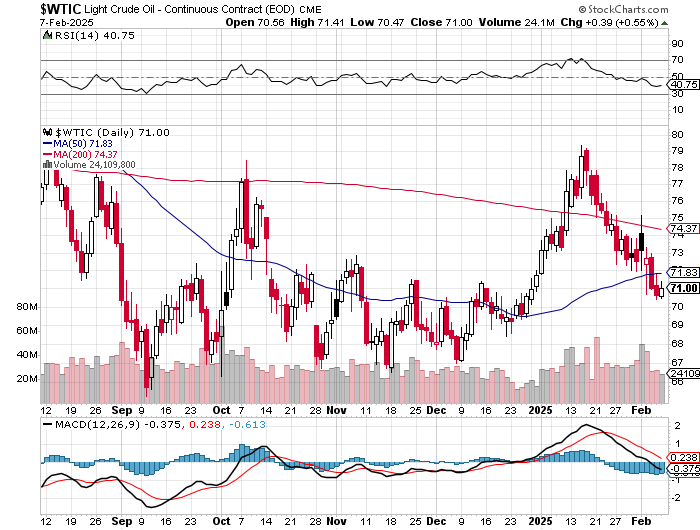

Natural gas [chart included] closed lower by an inconsequential 7 cents -- and finished the Friday trading session at $3.31/1,000 cubic feet. WTIC finally caught a bid...closing up 39 cents at $71.00/barrel...but still below any moving average that matters.

Here are the 6-month charts for the Big 6+1 commodities...courtesy of stockcharts.com as always and, if interested, their COMEX closing prices in their current front months on Friday should be noted. Click to enlarge.

There's been no let-up in the amount of gold and silver being flow in from London...as it has continued without a break all week long. As mentioned further up, there have already been a record [or very close to it] 55,127 COMEX gold contracts issued and stopped so far in February -- and that number in silver 3,327 contracts...with lots more open interest to go before the month is done.

Of course more contracts are being added to both on a daily basis -- and considering the fact that we are in uncharted territory from a delivery perspective, I'm not about to speculate as to what the final numbers will be by First Notice Day for March...which is still 14 business days away. But whatever those February numbers show, they'll be new high-water marks in gold -- and a record by a country mile for a non-scheduled delivery month for silver.

I'm also watching March open interest in gold...a non-scheduled delivery month in it...which has been skyrocketing since the beginning of the month -- and I'm already wondering if March silver will show an explosion of deliveries, like it's been for gold in February.

As I said in this space last week, the rush for immediate delivery/physical possession has kicked into overdrive...but so far the cargo planes full of bullion from the LBMA and the BofE have never failed to arrive at the various COMEX depositories in New York. Regardless of that, it's obvious that there is stress in these markets -- and how long the boys in London can keep up this 'business as usual' attitude in London, remains to be seen.

And as far as stress is concerned, those short gold and silver in COMEX futures, call options contracts -- and in the OTC market...are looking at unbooked/unrealized margin losses well north of $30 billion. Ted Butler would be aghast if he could see what the precious metal markets look like today -- and would have to do a major rewrite of his 'Bonfire of the Silver Shorts' essay...now 17 months old. I can only fantasize about what he would think about the unprecedented 74,518 contracts that his raptors are now short in gold.

A month or so ago, I [nor anyone else for that matter] could have ever imagined the drama that's currently unfolding in both silver and gold... especially the speed of it. Everyone up and down the physical supply chain was caught completely flat-footed -- and now they're scrambling. It now has all the hallmarks of a 'run on the banks'...except this time it's for physical metal...as those long, panic in their efforts to get metal in hand.

The interesting thing about this from a Daily Delivery Report perspective is that those who are long -- and demanding immediately delivery, are exposing those entities that are going short against them -- and if any further proof was needed that it was the big bullion banks...it's laid bare on a daily basis in this report. But its also the big bullion banks that are the large long/stoppers as well. It appears to be every bullion bank for itself [along with their clients] in the mad scramble for physical.

But as supplies dwindle in the face of this insatiable demand, the ability for the paper hangers in New York to keep their prices under wraps as the process continues, will become even more tenuous as time passes. And as you are more than aware from the daily price action, their efforts to keep them in line are now over-the-top blatant.

Whether or not this is the beginning of a hopefully controlled unwind of the price management scheme is still open for debate...but it certainly feels like we're only one delivery accident away from force majeure from one or more parties.

A non-linear event such as this would blow the market wide open -- and the melt-up in prices would begin -- and the melt-down and bankruptcy of those short the market would happen in days, if not hours...as they would be faced with daily or even hourly requests for more margin money.

According to Ted Butler, it happened to Bear Stearns back in 2008 when they couldn't meet a $2 billion margin call -- and had to be bailed by JPMorgan at the request of the Fed. Based on the $30+ billion margin call hole that the shorts are in now, I suspect one or more of them are close to a 'Bear Stearns moment' of their own.

Will the Fed save them? Who knows. Maybe they're already propping up the 'too big to fail' bullion banks as I write this, in order stave off the inevitable. But when the margin call losses begin to pile up exponentially, everyone will become to big to bail at some point.

That's why closing the COMEX -- and by extension, the LBMA...remains the only options left to save the shorts. If they don't -- and the Fed can't/won't save them...then that time will have arrived, as I've spoken of countless times over the last couple of decades, that "the world's financial system will be a smouldering ruin within five business days"...or maybe even less.

Of course the world's central banks will fight this hammer and tong. But then again, maybe not, as I've never quite been able to get David Rogers Webb's 'The Great Taking' out of my mind.

We are living through an historic moment in the world's financial and monetary systems. How it unfolds, or how long it takes -- and what the end of look like when it finally appears out of the wreckage, is unknown to everyone... including this writer.

But I suspect, as I and others have said before, it will manifest itself like Hemingway's description of bankruptcy..."slowly at first, then suddenly"...with that "suddenly" moment appearing to get closer with each passing day.

As always, I'm still "all in" -- and will remain so to whatever end.

I'm done for the day, the week -- and I'll see you here on Tuesday.

********

More from Silver Phoenix 500