Silver Short Squeeze Coming?

share

share

share

share

share

share

share

share

share

share

The Federal Reserve cut interest rates for the first time in over four years in September, sending gold past a record-setting $2,500 an ounce. The aggressive half-percentage-point reduction was in response to the Fed’s significant progress in bringing down inflation, as well as a slowing US economy evoking recession fears.

Gold’s rally, which started in mid-February, has been underpinned by increased geopolitical risks, the upcoming US election, central bank buying, and slowing ETF sales. It last traded at $2,744 an ounce, up 37% so far in 2024.

But silver has done even better, notching a YTD gain of 46%. Spot silver is now worth $33.67, as of Monday, 20:30 New York time. Last Tuesday it hit $34, the highest level since 2012.

Silver looks ready to rip — Richard Mills

Silver has benefited mostly due to physical buying in India and China. So-called “paper silver” has also been a factor. In July, two months of outflows reversed to inflows.

The Globe and Mail reported on Monday the 28th that silver ETFs saw the strongest rise amongst precious metals exchange-traded funds, with the iShares Silver Bullion ETF (SVR) and Purpose Silver Bullion Trust ETF (SBT.B) posting last week gains of 3.40% and 3.96% respectively.

October has been the best month on record for gold ETFs.

Source: Kitco

Source: Kitco

Source: Kitco

Price revisions

After silver struck a near 12-year peak on Monday, Oct. 21, Citi Research revised its six to 12-month forecast for silver prices upward to $40 per ounce from $38/oz.

UBS Bank is also bullish on silver, with the caveat that the gold-silver ratio rose above 85:1 (1 gold ounce to 85 silver ounces) in September after hitting lows of around 73X in May. (The higher the ratio, the more silver is considered to be undervalued compared to gold.)

“Despite this, we maintain our view that silver is set to benefit from a rising gold price environment, which is aligned with Fed policy easing,” analysts at the bank said. “Our expectation that the silver market will remain in deficit over the coming years implies continuous declines in above-ground inventories, which should help fundamentally underpin prices as well as act as a tailwind for investor interest.”

“We see silver outperforming gold over 12 months, with the potential for its ratio to test the long-term average of just below 70X.”

Banks face billions in losses

The unexpected price surge has put five US banks at risk of substantial losses due to their large silver short positions.

A “short squeeze” refers to a situation where an individual or legal entity sells an asset in the future without owning it first, in the hope of buying it back later at a lower price to make a profit. However, if the price of this asset increases instead of falling as expected, this individual or legal entity is forced to buy it quickly to honor the delivery of their forward sale. This hasty buying movement then contributes to accentuating the rise in prices — Goldbroker.com, ‘A Massive Short Squeeze on Gold’, Oct. 28, 2024

The Commodities Futures Trading Commission reported last week, via Yahoo Finance, that open interest in silver futures contracts has reached 141,580 contracts, each representing 5,000 ounces.

This amounts to approximately 707.9 million ounces, nearly equaling a year’s global silver production. With silver prices increasing by $1.84 per ounce, these short positions are now estimated to be underwater by $1.3 billion.

“This behavior undermines market integrity and could have far-reaching consequences for both the financial sector and industries that depend on stable silver prices,” said The Silver Academy.

The concentration of these short positions among just five U.S. banks has raised concerns among industry analysts. Critics argue that this level of short-selling artificially depresses silver prices, despite strong industrial demand from sectors like electric vehicles and solar panels.

“Silver is viewed as the relatively cheap sibling to gold, and as gold continues to reach fresh record highs and copper hits a 2 1/2 month high, traders took it through resistance at $32.50,” said Ole Hansen, head of commodities strategy at Saxo Bank A/S, according to a report by Bloomberg.

Concerns about market integrity and potential supply shortages have emerged, with some fearing a sharp price increase could force banks to buy back large quantities of silver, leading to significant losses.

The Jerusalem Post notes the disparity between paper and physical silver has reached staggering proportions, with paper claims exceeding physical silver by 400-450 to 1; COMEX registered inventories have reached historic lows; and less than 0.25% of futures contracts typically stand for delivery.

From Russia with love

Silver has not historically been associated with central banks. The relatively low price of silver versus gold means 70 to 80 times more silver than gold would have to be stored to attain value equivalency.

Those who have been following the trend of Russia accumulating gold to diversify its foreign exchange reserves as it dumps US Treasuries will not be surprised to learn that Russia has announced plans to add silver to its reserves.

The addition of silver to its already substantial holdings of gold, platinum and palladium, is outlined in the country’s Draft Federal Budget, which proposes an annual allocation of 51.5 billion rubles for precious metals purchases through 2027.

The report from The Silver Academy highlights several points:

- Historical Context: The move is compared to the 1973 Oil Embargo, with Russia exploiting control over a critical resource to exert geopolitical pressure.

- US Vulnerability: With the United States relying on imports for 80% of its silver needs, it’s particularly susceptible to supply disruptions.

- Global Implications: As other countries potentially follow Russia’s lead, we could witness an unprecedented setup for explosive growth in silver prices.

- Economic Strategy: The decision exposes vulnerabilities in the U.S. financial system, tracing back to the abandonment of the gold standard and the petrodollar system.

Jon Stuart Little, an analyst at The Silver Academy, warns of the potential ripple effects, especially if other countries follow Russia’s lead in building up their silver war chests:

“The ramifications of this shift extend beyond mere price movements. A significant revaluation of silver could disrupt existing financial paradigms, challenging the dominance of fiat currencies and potentially accelerating the transition towards a multi-polar economic world order.”

The Silver Academy’s report suggests that this move could be a game-changer for the precious metals market. “As the BRICS nations continue to explore alternatives to the dollar-centric financial system, including the possibility of a commodity-backed currency, silver’s role could become even more pivotal,” Little concludes.

Demand

Silver, like gold, is a precious metal that offers investors protection during times of economic and political uncertainty.

However, much of silver’s value is derived from its industrial demand. It’s estimated around 60% of silver is utilized in industrial applications, like solar and electronics, leaving only 40% for investing.

The lustrous metal has a multitude of industrial applications. This includes solar power, the automotive industry, brazing and soldering, 5G, and printed and flexible electronics.

Schiff Gold reported in May that silver demand in three sectors is expected to double in the next decade: industrial applications, jewelry production and silverware fabrication.

A report by Oxford Economics commissioned by the Silver Institute found that demand for these sectors is forecast to increase by 42% between 2023 and 2033.

The transition to an electrified economy doesn’t happen without copper and silver, which is why in my opinion they are among the most highly investable commodities now, and for the foreseeable future. The danger, for end users, and opportunity, for resource investors, of coming shortages for both metals, only strengthens my thesis.

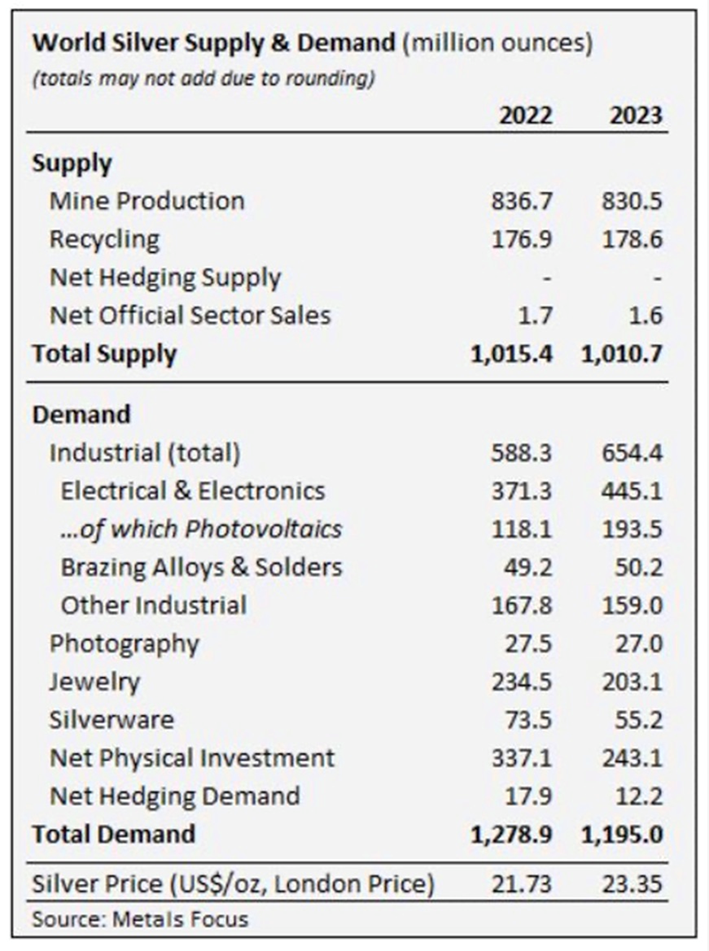

In a recent commentary, the Silver Institute said industrial demand rose 11% last year to a new record of 654.4Moz, smashing the old record set in 2022.

In fact demand exceeded supply for the third year in a row.

Solar

Higher-than-expected photovoltaic (PV) capacity additions and faster adoption of new-generation solar cells raised electrical & electronics demand by a substantial 20%, to 445.1Moz, the institute said.

As the metal with the highest electrical and thermal conductivity, silver is ideally suited to solar panels. A Saxo Bank report stated that “potential substitute metals cannot match silver in terms of energy output per solar panel.”

About 100 million ounces of silver are consumed per year for this purpose alone.

In May, a report by the International Energy Agency said global investment in solar PV manufacturing more than doubled last year to around $80 billion. This accounts for roughly 40% of global investment in clean-energy technology manufacturing.

Much of the growth is coming from, no surprise, China. The IEA says China more than doubled its investment in solar PV manufacturing between 2022 and 2023.

This is only going to continue.

According to Sprott, demand for silver from the makers of solar panels, particularly those in China, is forecast to increase by almost 170% by 2030, to about 273 million ounces — one fifth of total silver demand.

FX Street quotes a research paper by the University of New South Wales that found “solar manufacturers will likely require over 20% of the current annual silver supply by 2027. By 2050, solar panel production will use approximately 85–98% of the current global silver reserves.”

India loves silver

In the first four months of 2024 Indians imported more silver than they did in all of 2023 (a record 4,172 metric tons). Demand is being driven by rising solar demand and investor interest.

Texas vs Alberta

Solar and wind power have found an unusual recipient in Texas. The oil-rich state is home to the prolific Permian shale oil basin, and bleeds red for Republican.

Residents who are allowing wind farms on their private lands told The Globe and Mail they are not climate activists: For them, renewable energy is not a route to decarbonizing Texas’s economy, but an opportunity to broaden their sources of income through lease contracts with developers.

The article says Texas’s deregulated power market is a mecca for wind and solar power, in addition to battery storage. This has made the state one of the largest beneficiaries of green stimulus money from the Inflation Reduction Act. Since the IRA was passed, Texas has racked up USD$8 billion in clean-energy investments.

Since 2011, wind power has quadrupled to nearly 40,000 megawatts, or nearly 29% of total available generation. Solar power growth has surged from 70 MW in 2011 to 26,814 MW today. In 12 months, that could jump by another 56%. Battery capacity could more than double in the next year to over 19,000 MW.

Compare what’s happening in Texas to another oil-rich and politically conservative jurisdiction, Alberta. Last year, a renewables boom dried up when Premier Danielle Smith’s United Conservative Party government slapped a seven-month moratorium on new wind and solar applications, then imposed a series of restrictions on the industry.

Part of the rationale for Texas renewables is the state’s notoriously archaic power distribution system. In February 2021, a freak winter storm caused widespread power outages. While renewable-energy opponents seized on the crisis to blame wind and solar, reviews later showed the network collapsed under a combination of events, The Globe said, including natural gas and coal power plants that were not designed to withstand such harsh winter conditions.

Another test of the power grid came this summer, when Texas experienced a weeks-long heat wave. According to the article, The bright sunshine allowed solar generation to hit records of nearly 21,000 MW in August, about a quarter of peak daytime demand, according to energy data provider Grid Status.

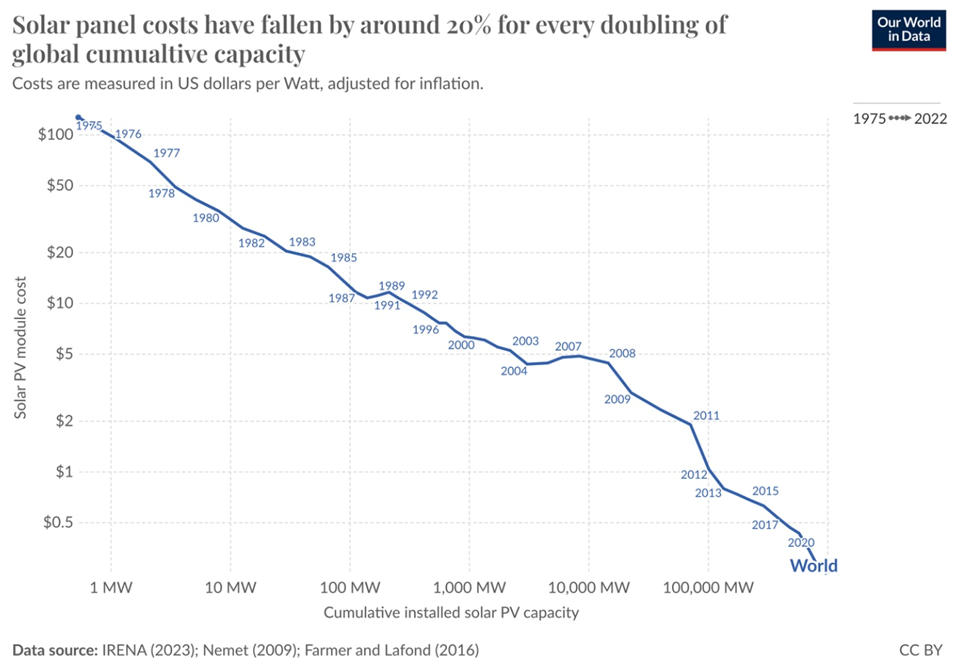

(Before we get too carried away with solar, there is a counter-point. The price of solar panels have fallen significantly over the years. According to Our World in Data, solar panel prices have fallen by 20% every time global capacity doubled. Solar photovoltaic costs have plummeted by 90% in the last decade, as the chart below shows. The substantial reduction can be attributed to several factors, including technological advancements, economies of scale, and increased competition among manufacturers, writes GreenMatch. China’s dominance in global solar module manufacturing has led to a significant oversupply, causing global solar panel prices to crash by 50%.)

Solid-state batteries

If the demand for silver in solar power doesn’t blow the doors off the silver price in the near future, it may be a change in battery technology that does it.

Kitco reported recently that Samsung has developed a new solid-state battery that includes silver as a key component.

The site quotes retired investment professional Kevin Bambrough saying:

“The key drivers that will ramp up demand for EVs are range, charge time, battery life and safety,” Bambrough said. “Samsung’s new solid-state battery technology, incorporating a silver-carbon (Ag-C) composite layer for the anode, exemplifies this advancement. Silver’s exceptional electrical conductivity and stability are leveraged to enhance battery performance and durability, achieving amazing benchmarks like a 600-mile range and a 20-year lifespan and 9-minute charge.”

Bambrough provided estimates showing there could be up to 5 grams of silver per cell in these batteries, meaning “a typical EV battery pack containing around 200 cells for a 100 kWh capacity could require about 1 kg of silver per vehicle.”

If his numbers are right, it could mean a major new demand driver for silver going forward. Even if 20% of electric vehicles were to adopt Samsung’s SS batteries, the annual demand for silver would be around 16,000 tonnes, against total current production of 25,000 tonnes.

Kitco cites a report that says Samsung is already working with big automakers to incorporate its SS battery technology into EV development, including an agreement with Toyota to begin mass production of SS batteries in 2027. Lexus vehicles are also scheduled to be among the first to adopt them.

The challenge is the cost. It’s around 3-4 times more expensive to manufacture SS batteries compared to lithium-ion and lithium-iron-phosphate batteries — not exactly a route to making EV sticker prices lower for cash-strapped and skeptical car buyers.

Also, battery-makers that currently have first-mover advantage in manufacturing automotive lithium-ion batteries aren’t going to suddenly switch to solid-state which requires significant cost outlays and additional silver supply purchases.

Miners are hoping to capitalize on the increasing demand for silver.

Coeur Mining recently completed an expansion of its Rochester mine in Nevada, which is set to become the largest source of US-mined silver.

Hochschild Mining is also looking to expand its silver operations, by securing permits for a silver project in Peru slated to start in 2027.

Increasing investor interest in silver is hiking the share prices of some of the major silver miners. Pan American Silver is up 59.7% year to date, Coeur Mining has more than doubled from $3.20 to $6.93, and Hecla Mining has risen from $4.69 to $7.02, a gain of 45.9%.

The Global X Silver Miners ETF (SIL) so far this year is up 47.5%.

Source: Yahoo Finance

Source: Yahoo Finance

Supply

On the supply side, global silver mine production fell by 1% to 830.5Moz in 2023. Output was constrained by a four-month suspension of operations at Newmont’s Penasquito mine in Mexico due to a strike; lower ore grades; and mine closures in Argentina, Australia and Russia.

Silver mined shortfall

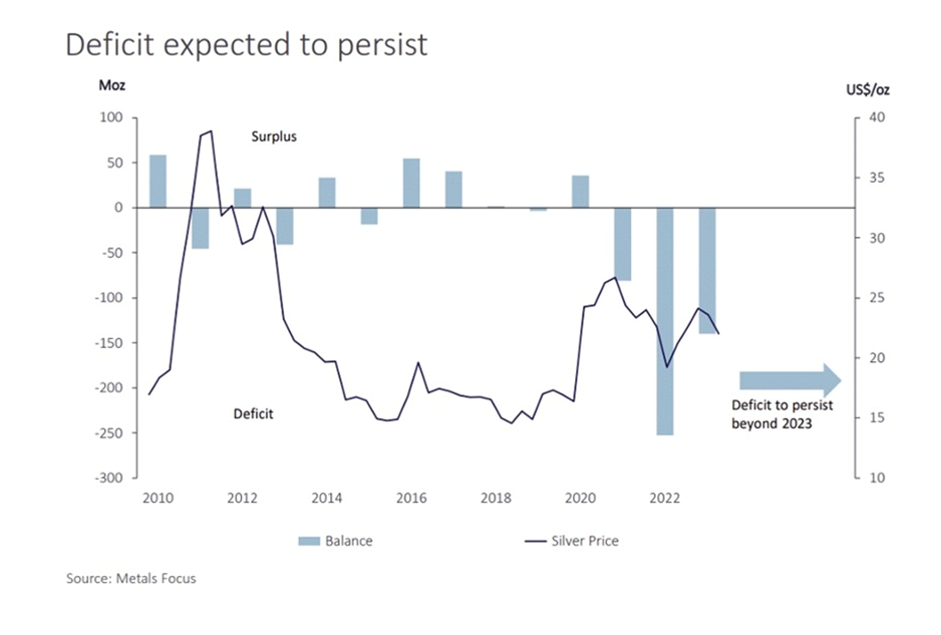

The Silver Institute reported a 184.3 million-ounce deficit in 2023 on the back of robust industrial demand.

The Silver Institute expects demand to grow by 2% this year, led by an anticipated 20% gain in the solar PV market. Industrial fabrication should post another all-time high, rising by 9%. Demand for jewelry and silverware fabrication are predicted to rise by 4% and 7%, respectively.

Total silver supply should decrease by 1%, meaning 2024 should see another deficit, amounting to 215.3Moz, the second-largest in more than 20 years.

In fact it’s the fourth year in a row that the silver market would be in a structural supply deficit.

The deficit actually fell 30% last year but at 184.3 million ounces it’s still massive. Global supply has been broadly steady at around 1 billion ounces but last year industrial silver demand grew 11%, reaching a new record of 654.4 million ounces. Usage was mostly in the green economy sector (renewable energy, electrification and decarbonization of the global transportation system).

Total silver demand was 1.195 million ounces compared to 1,010.7Moz of total supply, which included mine production of 830.5Moz (-1%) and recycling of 178.6Moz.

Money Metals recently asked: Can silver miners respond and restore the market balance?

The publication notes silver mine production peaked at 900.1 million ounces in 2016. Silver at that time was only $13.30 an ounce. Today, silver is $34/oz.

The problem is that silver miners have yet to respond to the higher price. According to Metals Focus, mine output this year will be 62.8Moz lower than the 2016 peak, a decline of 7%.

Why won’t silver production ramp up to meet the demand and take advantage of higher prices? Money Metals explains:

Metals Focus blames the price inelasticity on the fact that more than half of silver is mined as a byproduct of base metal operations.

“Although silver can be a significant revenue stream, the economics and production plans of these mines are primarily driven by the markets for copper, lead and zinc. Consequently, even significant increases in silver prices are unlikely to influence production plans that are dependent on other metals.”

About 28 percent of the silver supply is derived from primary silver mines, where production is more tightly tied to price. But silver mines face their own challenges including declining ore grades and rapidly rising mining costs.

Ore grades have fallen by about 22 percent, meaning the silver price has to rise that much to maintain margins.

Metals Focus summarized the cost challenges facing silver miners.

“Rising production costs have further constrained silver supply. Despite higher silver prices, operating costs in many cases have outpaced revenue growth, leading to little or no improvement in operating cash flow for silver-focused mining companies. Moreover, capital expenditure requirements have continued to rise, with mining cost inflation requiring increasing investment just to maintain current production levels. As a result, many silver miners have been free cash flow negative in recent years.”

If silver prices rise as projected, mines will reach a threshold where higher revenues translate into improved free cash flow.

“At that point, the future of primary silver mine supply will depend on how management allocates capital.”

Even if mining companies allocate significant resources to finding new sources of silver and developing new mines it will take time for production to ramp up and ease the supply shortage. According to Metals Focus, “It is implausible that new production could balance the current deficits over the short to medium term. For those shortfalls to end, we are instead dependent on recycling and demand to react to the forecast price rally.”

For the next few years at least, we will have to depend on drawdowns of above-ground stocks to meet the supply deficit.

Conclusion

The silver price is up 46% year to date.

Some are led to believe that a looming “silver squeeze” could be the investment opportunity of a generation. An article in Jerusalem Post maintains that “for decades, a small group of powerful banks has maintained massive short positions in silver, effectively acting as a cartel to control and suppress prices.”

Earlier it was stated a silver squeeze could happen if the silver price suddenly spiked and five US banks were forced to buy silver quickly to honor the delivery of their forward sale, leading to a further price rise.

I don’t think it’s possible to squeeze the silver shorts.

Endeavour Silver explains…

“Silver is the only common metal that is mined primarily as a byproduct of other metals. Fully 70% of all silver production is a byproduct of copper, lead-zinc and gold mines. But those copper, lead-zinc and gold miners tend to be very large and diversified global mining companies who are happy to sell forward or hedge their byproduct silver production so as to lock in that revenue and leave themselves unhedged to their primary metals.

Who buys these forward sales? The bullion bankers, or commercials, whose business is not going long or short anything but rather charging a fee for their services.

When a bullion banker goes long physical silver by entering into a contract to buy silver from a large, diversified mining company, they automatically go “short” in the paper market to balance their position. When the silver price rises, the value of the commercials physical silver holdings, including future holdings, also rises so they simply cover their hedge and reset it at a higher price. This they can do ad infinitum so it is neither feasible or even possible to squeeze the silver “shorts”.

If anyone were to try to squeeze the silver paper “shorts”, the biggest winner by far would be the commercials because of their physical “longs”.” Endeavour Silver

Citi Research and UBS Bank have both revised their price targets upward, with UBS forecasting silver will continue to outperform gold.

Among the demand drivers for silver are solar power, electronics, jewelry and silverware. Silver is used in a number of military applications including radar, night vision equipment and munitions.

Solid state batteries are still in their infancy but they are expected to use a lot of silver: “a typical EV battery pack containing around 200 cells for a 100 kWh capacity could require about 1 kg of silver per vehicle.”

Russia’s announcement that it is planning on adding silver to its metal reserves is another new source of demand for silver. As other countries (like the expanded BRICS) follow Russia’s lead, it could be the setup for explosive growth in silver prices.

Meanwhile, the silver market in 2024 is in deficit and is expected to be for the fourth year in a row.

The Silver Institute expects demand to grow by 2% this year, led by an anticipated 20% gain in the solar PV market (with the current Chinese oversupply working through the market I expect panel manufacturing to slow). Industrial fabrication should post another all-time high, rising by 9%. Demand for jewelry and silverware fabrication are predicted to rise by 4% and 7%, respectively.

Total silver supply should decrease by 1%, meaning 2024 should see another deficit, amounting to 215.3Moz, the second-largest in more than 20 years.

Silver miners can’t seem to mine more silver to meet the rising demand, despite higher prices. Part of the reason has to do with other metals; more than half of silver is mined as a byproduct.

Silver is mostly a byproduct of other mining operations like copper, lead, zinc and gold, but even if production of these metals rises significantly, it arguably won’t be enough to correct the silver deficit. Zinc for example has risen 17% year to date, but lead prices have been all over the map, currently trading at $2,008.50 per tonne compared to $2,028.80 at the start of the year. Gold as mentioned is up 37% YTD, but gold mines only represented 13.7% of global silver production in 2023.

Silver ore grades have fallen by nearly a quarter, while mining costs have risen. For the next few years, Metals Focus says we will have to depend on drawdowns of above-ground stocks to meet the supply deficit. TD Bank recently said that growing demand could wipe out silver’s above-ground stocks within one to two years.

In 2023, mine supply of 830.5 million ounces failed to meet demand of 1.195Moz. Only by recycling 178.6Moz could demand be satisfied, meeting our definition of peak silver.

I continue to maintain my belief that junior resource companies offer the best leverage to rising commodity prices, including silver.

Source: Yahoo Finance

Source: Yahoo Finance

Always conduct your own due diligence.

*********

share

share

share

share

share

More from Silver Phoenix 500