Why Max’s CESAR Is Our Favorite Copper-Silver Play

share

share

share

share

share

share

share

share

share

share

Copper and silver are essential metals when it comes to the transition from fossil-fueled transportation and power generation to electricity-based systems.

A good argument can be made that to get the electrical juice flowing from any kind of energy source to any type of energy storage device, you have to have copper and silver.

Copper is one of the most important metals with more than 20 million tonnes consumed each year across a variety of industries, including building construction (wiring & piping,) power generation/ transmission, and electronic products manufacturing.

In recent years, the global transition towards clean energy has stretched the need for the red metal even further. More copper will be required to feed our renewable energy infrastructure.

Electric vehicles use triple the amount of copper as gasoline-powered cars. There’s copper in the wiring, lithium-ion battery, motor and cables. Charging stations will also need copper.

President Biden has set a goal of 500,000 public charging stations by 2030, a five-fold increase from the 100,000 in place already. A charging station takes up to 8 kg of copper, depending on how long it takes to charge the EV.

Millions of feet of copper wiring will be required for strengthening the world’s power grids, and hundreds of thousands of tonnes more are needed to build wind and solar farms.

Silver, like gold, is a precious metal that offers investors protection during times of economic and political uncertainty.

However, much of silver’s value is derived from its industrial demand. It’s estimated around 60% of silver is utilized in industrial applications, like solar and electronics, leaving only 40% for investing.

The lustrous metal has a multitude of industrial applications. This includes solar power, the automotive industry, brazing and soldering, 5G, and printed and flexible electronics.

As the metal with the highest electrical and thermal conductivity, silver is ideally suited to solar panels. A Saxo Bank report stated that “potential substitute metals cannot match silver in terms of energy output per solar panel.”

About 100 million ounces of silver are consumed per year for this purpose alone.

The transition to an electrified economy doesn’t happen without copper and silver, which is why in my opinion they are among the most highly investable commodities now, and for the foreseeable future. The danger, for end users, and opportunity, for resource investors, of coming shortages for both metals, only strengthens my thesis.

Silver

The Silver Institute reported a 184.3 million-ounce deficit in 2023 on the back of robust industrial demand.

In a recent commentary, SI said industrial demand rose 11% last year to a new record of 654.4Moz, smashing the old record set in 2022.

In fact demand exceeded supply for the third year in a row.

Higher-than-expected photovoltaic (PV) capacity additions and faster adoption of new-generation solar cells raised electrical & electronics demand by a substantial 20%, to 445.1Moz, the institute said:

This gain reflects silver’s essential and growing use in PV, which recorded a new high of 193.5 Moz last year, increasing by a massive 64 percent over 2022’s figure of 118.1 Moz. Underpinning these overall gains was the limited scale of thrifting and substitution, as silver remains irreplaceable in many applications.

Chinese silver industrial demand rose by a remarkable 44 percent to 261.2 Moz, primarily due to growth for green applications, chiefly PV. Last year, China’s rapid expansion of PV production accounted for over 90 percent of global panel shipments. Industrial demand in the United States stood at 128.1 Moz, essentially flat over 2022, while Japan’s industrial offtake was also basically unchanged at 98.0 Moz.

On the supply side, global silver mine production fell by 1% to 830.5Moz in 2023. Output was constrained by a four-month suspension of operations at Newmont’s Penasquito mine in Mexico due to a strike; lower ore grades; and mine closures in Argentina, Australia and Russia.

Source: The Silver Institute

The Silver Institute expects demand to grow by 2% this year, led by an anticipated 20% gain in the PV market. Industrial fabrication should post another all-time high, rising by 9%. Demand for jewelry and silverware fabrication are predicted to rise by 4% and 7%, respectively.

Total silver supply should decrease by 1%, meaning 2024 should see another deficit, amounting to 215.3Moz, the second-largest in more than 20 years.

Silver is up 10% so far this year in a metal market that has traded sideways for the past three years. (Silver jumped in 2020 along with gold, on account of the pandemic.)

Source: Kitco

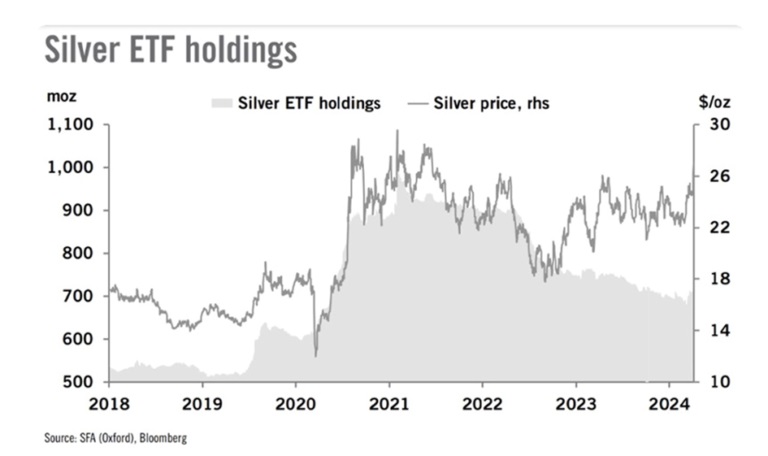

Who’s buying all the silver? India and silver-backed ETFs.

India in February purchased a whack of silver bullion, with silver imports surging 260%. The country bought 2,295 tonnes compared to just 637t in January — a new monthly record.

Putting that into perspective, it’s about 70 million ounces, more silver than the US Mint produced in American Silver Eagle coins over the past three years combined.

Kitco reported on April 8 that silver appears to be benefiting from both investment and industrial demand, and that silver is following copper, also an industrial metal, higher due to a tight copper market. Many investors are choosing to ride silver in an ETF investment vehicle. Kitco quoted precious metals analysts at Heraeus saying,

“Silver is a higher beta commodity than gold, so if retail investors show more interest as ETF holdings rise then it could outperform gold,” they noted. “Additionally, and in contrast to the gold market, silver investors re-entered the market for ETFs, with 10.7 moz of inflows in the last fortnight, taking total silver ETF holdings 3% higher year-to-date at 724 moz.”

The analysts said that industrial demand for silver is also expected to rise this year, based on “recent strong manufacturing data from the US and China” in addition to burgeoning Chinese solar installations.

Copper

On April 26 copper hit $10,000 a ton, setting a new two-year high a few days after BHP offered to buy Anglo American.

Despite the potential tie-up, investors continue to wager that miners will struggle to produce enough red metal to meet demand.

Source: Kitco

The main reason copper has been climbing is due to tighter supply as demand steadily increases — something we at AOTH have been pounding the table about for years. In fact we were the first resource investing newsletter to identify the coming supply deficit, which wasn’t supposed to happen until 2025 but is already here.

While some dismissed our warnings, others are now acknowledging we were right. Part of the reason for the price surge are sliding stocks in LME registered warehouses, which at 121,200 tonnes have dropped more than 35% since October, Reuters said.

The other reason is less mine supply coming to market.

Production concerns began last year, when the government of Panama ordered First Quantum Minerals to shut down its Cobre Panama operation, removing nearly 350,000 tonnes from global supply.

A strike at another large copper mine, Las Bambas in Peru, temporarily halted shipments. Copper specialist Anglo American says it is scaling back output by about 200,000 tons, owing to head grade declines and logistical issues at its Los Bronces mine.

Half of all copper mining is at risk of drought due to climate change. (Bloomberg, April 30, 2024)

Chile’s copper output has been dented by a long-running drought in the country’s arid north. State miner Codelco’s 2023 production was the lowest in 25 years.

There are also concerns about Zambia, Africa’s second largest copper producer, where drought conditions have lowered dam levels, creating a power crisis that threatens the country’s planned copper expansion.

According to a report by PricwaterhouseCoopers LLP, by 2050 more than half the world’s copper mines will be in areas exposed to drought risk deemed significant, high or extreme. Drought exposure is even higher for lithium and cobalt.

Back to the BHP-Anglo American deal, BHP Group is reportedly considering making an improved offer after Anglo American’s shareholders rejected the USD$39 billion initial proposal as undervaluing the company.

One media source said the news highlights a fundamental disconnect in the industry, i.e., that miners aren’t building enough copper mines:

The biggest producers all want to increase copper output to take advantage of rising demand in electric vehicles, grid infrastructure and data centers. BHP has made its $39 billion proposal to buy Anglo American in large part because the world’s biggest miner wants to grow in copper.

Yet, that bullishness still isn’t translating into the huge investments involved in developing new pits and shafts and associated infrastructure. A successful takeover would make BHP the biggest copper producer with about 10% of the market, but it won’t make any difference toward meeting the world’s supply needs.

Indeed, one major/ mid-tier copper miner buying another only “shifts” copper reserves from one balance sheet to another. It doesn’t actually add any new copper to global supply.

Some of the world’s largest mining companies, market analysis firms and banks are warning that by mid-decade, a massive shortfall will emerge for copper, which is now the world’s most critical metal due to its essential role in the green economy.

According to CRU Group, production from existing mines is set to fall sharply in coming years, and miners would need to spend over $150 billion between 2025 and 2032 to fulfill the industry’s supply needs.

“There is a clear and compelling need for additional mine capacity to be brought online,” Bloomberg quotes William Tankard, principal analyst for base metals at CRU. “The gauntlet is being laid down at the feet of the miners, and it’s going to be exceptionally challenging to deliver.”

Two reasons we aren’t extracting more copper are costs (incentive pricing in the copper industry is considered to be anywhere from US$11,000/t to 15,000/t) and regulatory delays.

In North America, it can take up to 20 years for a mine to go from discovery to production.

The difficulty in building new copper mines makes it understandable that companies like BHP would rather just acquire other companies’ mines rather than build their own. They aren’t doing anything to alleviate the copper deficit, though, and eventually they’re going to run out of companies to buy. There are only so many firms with mines producing over 200,000 tonnes a year.

A better strategy, imo, is to buy new copper “in the ground” owned by junior resource companies, whose role in the mining food chain is to acquire projects, make discoveries and hopefully advance them to the point when a larger mining company takes it over. Discoveries won’t be made if juniors aren’t out in the bush looking at rocks.

Not just any discovery will do; the deposit must be of sufficient size and scalabity to interest a major.

Max Resource Corp (TSXV:MAX; OTC:MXROF; Frankfurt:M1D2)

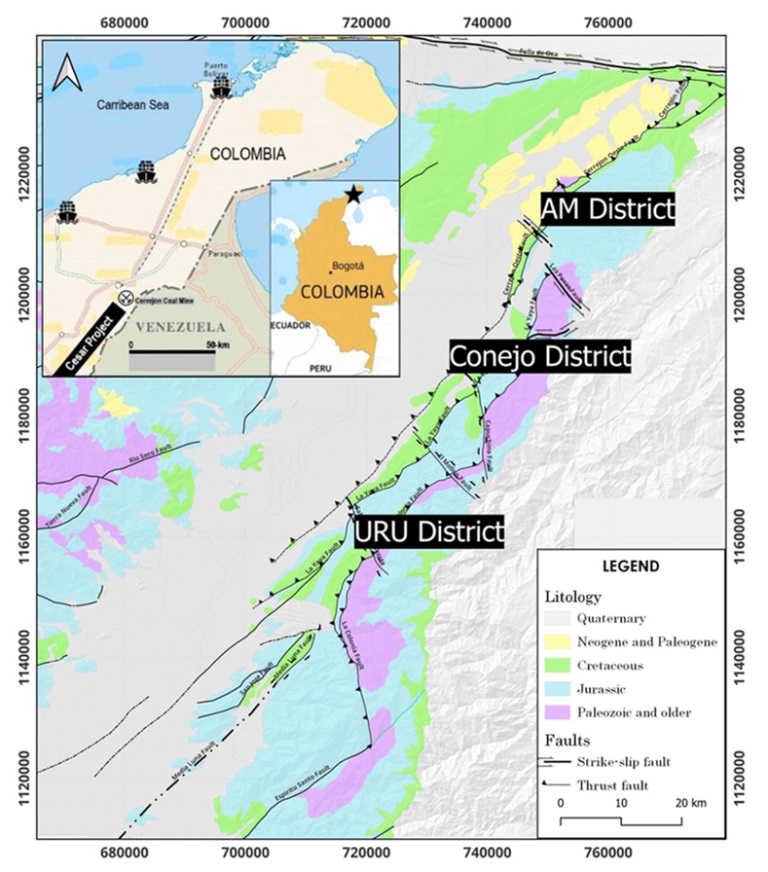

Max has made significant progress over the last year at CESAR, the sprawling copper-silver project it is developing in northeastern Colombia.

The property is situated along the copper-silver-rich Cesar Basin. This region provides access to major infrastructure resulting from oil & gas and mining operations, including Cerrejon, the largest coal mine in South America held by Glencore.

Vancouver-based Max was the first to recognize the potential for the Cesar Basin. Its land package now spans more than 1,150 km of geology prospective for sedimentary-hosted copper and silver deposits. Max’s 20 mining concessions total over 188 square km.

Field teams have so far identified 28 targets across three districts of the 120-km Cesar copper-silver belt: AM, Conejo and URU.

Location and scale of the CESAR copper-silver project, NE Colombia

Exploration to date

Starting in the far north of the Jurassic-aged basin, classic stacked red-bed outcrops with extensive lateral continuity have been rock-sampled within the AM District. Highlight values of 34.4% copper and 305 g/t silver have been documented in these sedimentary red-bed sequences.

The company confirmed that stratiform mineralization continues at depth with two scout drill holes completed.

The Conejo District, midway south, demonstrates mineralization at the contact of intermediate and felsic volcanics which outcrops over 3.7 km. The average of surface samples at a 2.0% cut-off comes in at 4.9% copper.

To the far south, 2022 inaugural drilling was initiated at two mineralized surface exposures, each located 750m apart and within the URU District’s 20-km-long, 2-km-wide mineralized target area.

This URU drill program was the first opportunity to test continuity of the structurally controlled copper-silver mineralization within the volcanic host rocks in the sub-basinal environment of the Cesar sedimentary basin.

At URU-C, a 9.0m of 7.0% copper and 115 g/t silver surface discovery was confirmed at depth by drill hole URU-12, which intersected 10.6m of 3.4% copper and 48 g/t silver. At the URU-CE target, 750m to the east, 19.0m of 1.3% copper discovered in outcrop was confirmed by drill hole URU-9, which intersected a broad zone of copper oxide returning 33.0m of 0.3% copper from 4.0m, including 16.5m of 0.5% copper.

Additional ground acquired

In 2022, Max executed a two-year co-operation agreement with Endeavour Silver to help Max expand its land holdings at CESAR. Endeavour holds an underlying 0.5% NSR. It’s important to note that Max does not dilute its land position through the agreement; it retains 100% ownership of the ground it controls, and future mineral tenures.

The company announced on Nov. 8 that it has secured 12 more applications for mining concessions covering over 132 square kilometers. It means CESAR now spans 120 along strike, from the previous 90 km, in a north-northeast/ south-southwest direction.

Max has also acquired the royalties associated with 19 mining concessions and 31 mining concession applications at CESAR.

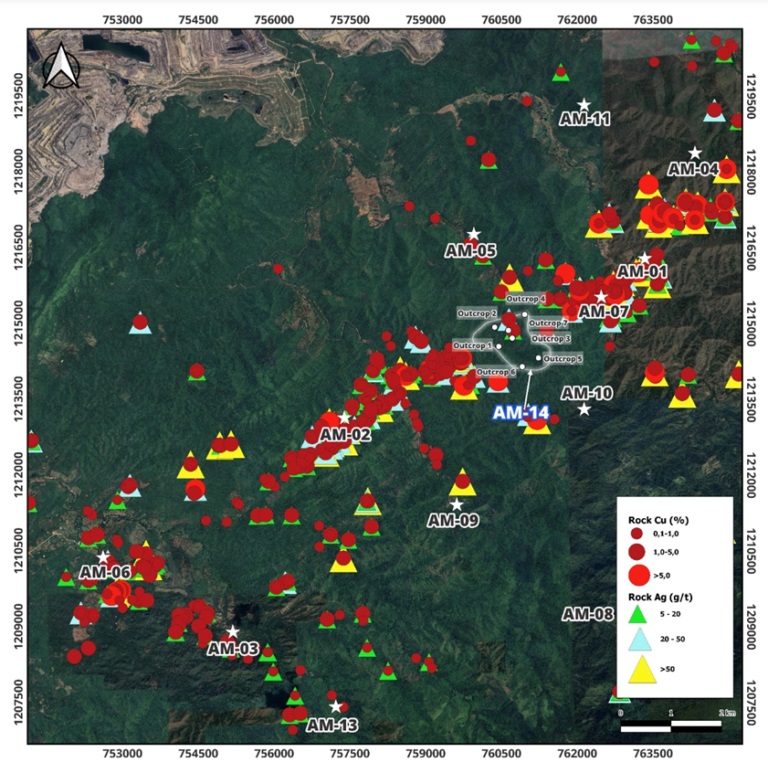

AM District

In September, Max announced the discovery of a new mineralized outcrop, AM-08, about 7 km southeast of the AM-07 discovery, within the most northerly AM District.

Max Resource Discovers New Copper & Silver Target at CESAR

In late October, interpretation of preliminary airborne magnetic-radiometric survey data identified four new targets within the AM district. The targets were AM-9 to AM-12.

In February the company announced it found an additional series of five mineralized outcrops within the AM District. Collectively they are known as target area AM-14.

Max Resource Discovers 5 New Copper & Silver Targets at CESAR

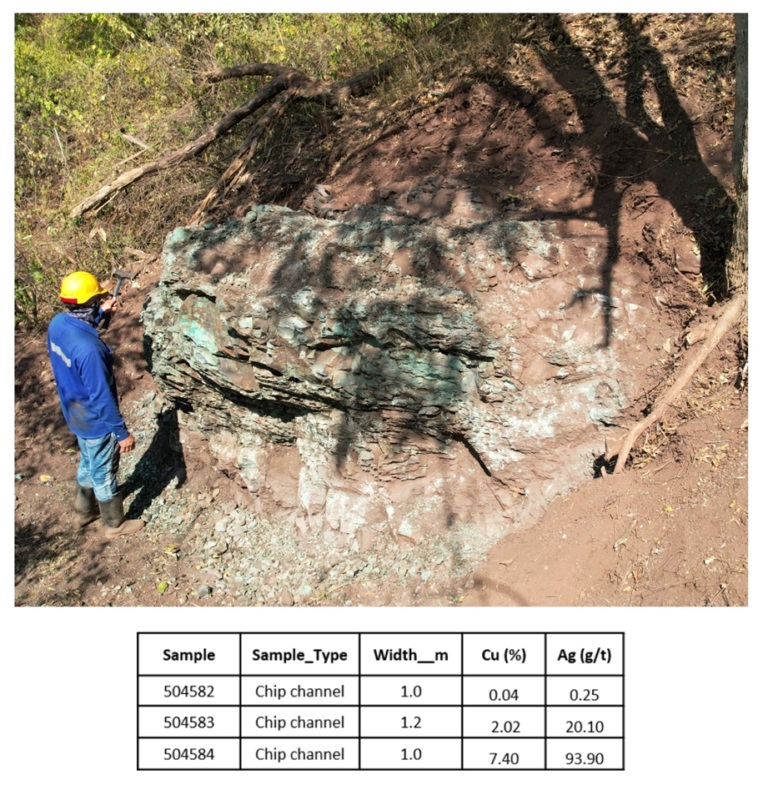

Assays released in March highlighted 2.2% copper and 12.8 grams per tonne silver over 5.2m, and 4.8% Cu and 53.6 g/t Ag over 2.2m.

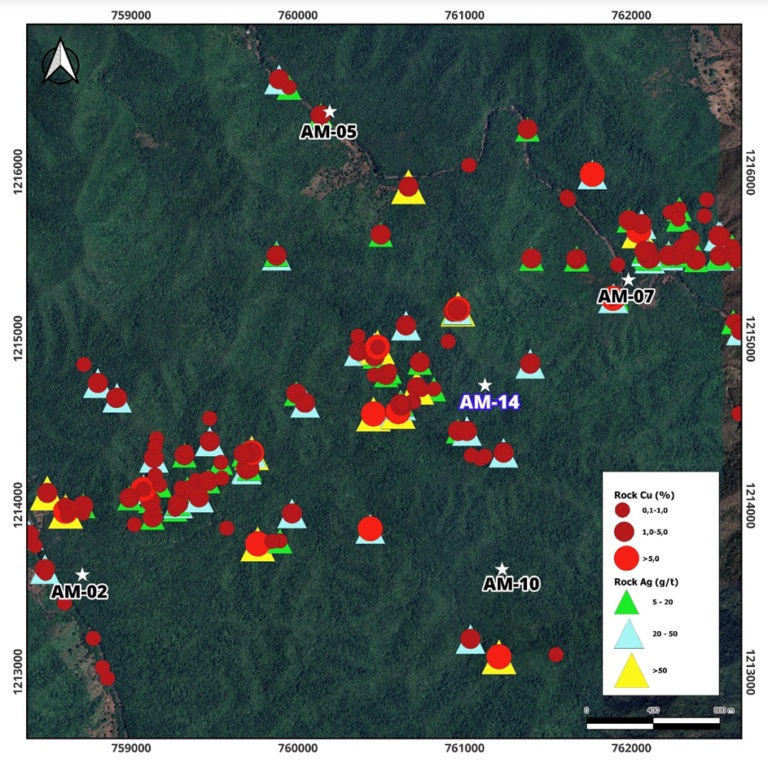

According to Max, the assays confirm that copper-silver mineralization at CESAR is extensive and thick. AM-14 lies along a 15-km corridor of mineralization (Fig. 1), with four distinct mineralized horizons (Fig. 2).

Figure 1: 15-km corridor of high-grade copper-silver mineralization at AM

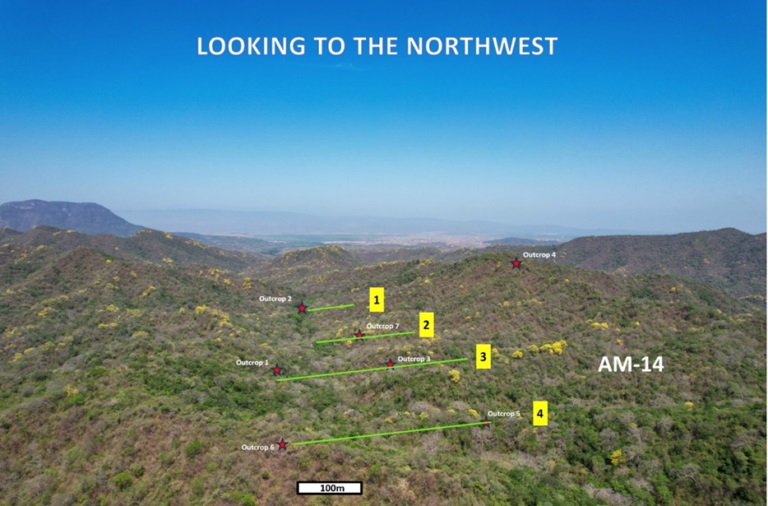

Figure 2: Location of four mineralized horizons at AM-14

“We are elated to confirm that high-grade copper and silver assay results over substantial widths from the numerous outcrops at AM-14 not only confirm our thesis of Kupferschiefer-style mineralization, but also substantiate our belief that the 15-km corridor of mineralization has the potential to host a significant deposit,” MAX’s CEO Brett Matich said in the March 25 news release.

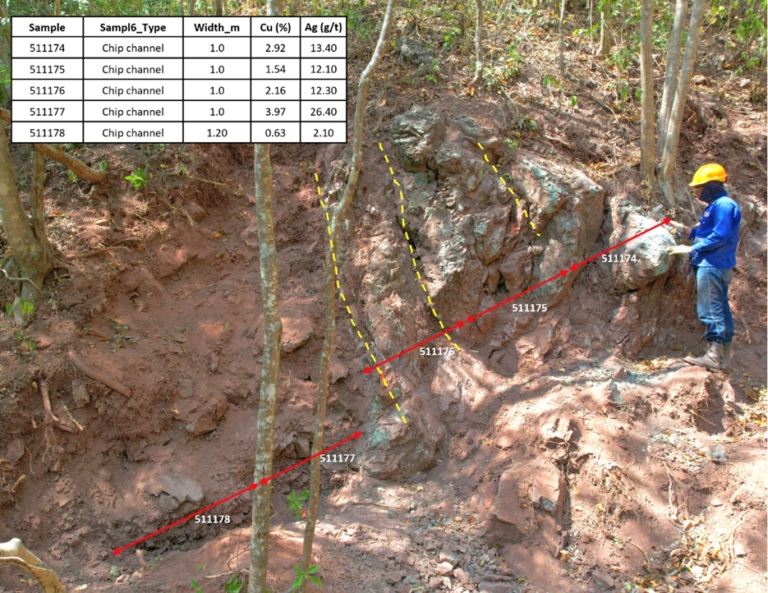

Max says the mineralization at target AM-14 is hosted in layers of medium- to fine-grained sandstone rich in organic material. The copper-silver bearing horizons are within a 700-meter-thick package of interbedded sedimentary rocks that strike 240⁰ to 260⁰ and dip 30⁰ to 45⁰ northwest. Chalcocite, malachite and azurite are the most abundant copper minerals observed in the outcrop. (Fig. 4 and 5)

According to the company, all four of the outcropping mineralized beds are open along strike, with copper-silver-bearing sandstone horizons traced for up to 285m along strike. Crews continue to map the area with the goal of extending the footprint of mineralization. Assays from the two remaining outcrops discovered at AM-14 are pending.

Figure 3: Results from recently discovered mineralized outcrop target AM-14

Figure 4: Newly discovered mineralized outcrop at target AM-14

Figure 5: Recent assay results at target AM-14

Target evaluation

Max has identified and is evaluating 28 targets along the 120-km-long belt for potential drill testing. The company is focused on expanding, refining, and prioritizing these targets in preparation for a drill program. Initial efforts have been concentrated on those targets with the greatest size potential with work that includes the following field activities:

- Systematic chip and channel sampling of the mineralized outcrops.

- Detailed geological and structural mapping of each showing.

- Target scale prospecting and soil sampling.

- Airborne magnetic/radiometric surveys.

- Regional exploration

While Max has demonstrated that the Cesar Basin is fertile for copper-silver mineralization over a large area, only a fraction of the basin has been explored. Therefore, Max says its geological teams are dedicated to regional exploration, with the goal of discovering additional copper-silver prospects over 1,000 square kilometers.

Max Resource Corp.

TSXV:MAX; OTC:MXROF; Frankfurt:M1D2

Cdn$0.21 2024.04.30

Shares Outstanding 161.9m

Market cap Cdn$36.9m

MAX website

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

*********

share

share

share

share

share

More from Silver Phoenix 500