A Minsky Moment Strikes Silver

share

share

share

share

share

share

share

share

share

share

Was this a one-off decline, or a sign of things to come?

With silver plunging by nearly 5% on May 11, its descent highlights the dangers of momentum investing. Moreover, we warned on May 5 that one-sided positioning often elicits a race for the exits. We wrote:

Rate cuts and QE are illogical when the PMIs, inflation, and employment are accelerating. Therefore, it’s likely only a matter of time before a Minsky Moment strikes the precious metals market.

So, while we may be approaching a turning point, the silver price needs to decline substantially to reflect its fundamental value. Thus, more weakness should be on the horizon.

Speaking of which, we have been consistent in our thesis that interest rates are too low to suppress demand and cure inflation. And while the crowd disagrees, the Fed should have to remain hawkish for longer than expected, as it did in 2021 and 2022.

Bridgewater Associates Expectation

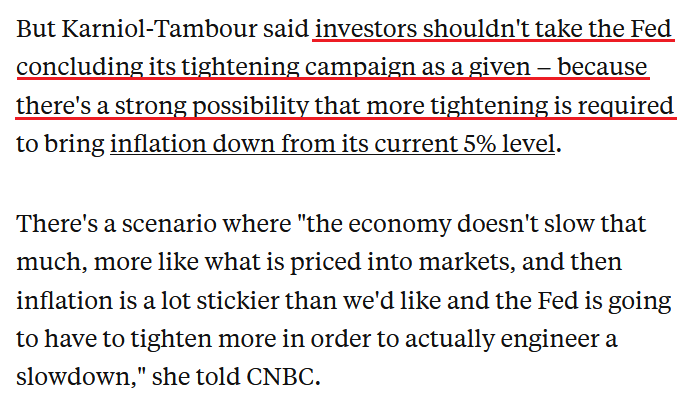

Furthermore, Bridgewater Associates' co-CIO Karen Karniol-Tambour expects a similar outcome. For context, Bridgewater Associates is the largest hedge fund in the world. She said on May 3:

“My view is that the economy needs to slow. I don't know if the tightening the Fed has done is enough to slow the economy sufficiently to really bring inflation back down to what its target is…. It's one of the most dangerous and bad times for risk assets that we've seen in decades.”

Consequently, while the crowd assumes QE is a done deal, Karniol-Tambour does not share their enthusiasm.

Please see below:

To that point, Bridgewater Associates’ CIOs explained why on Apr. 14. They wrote:

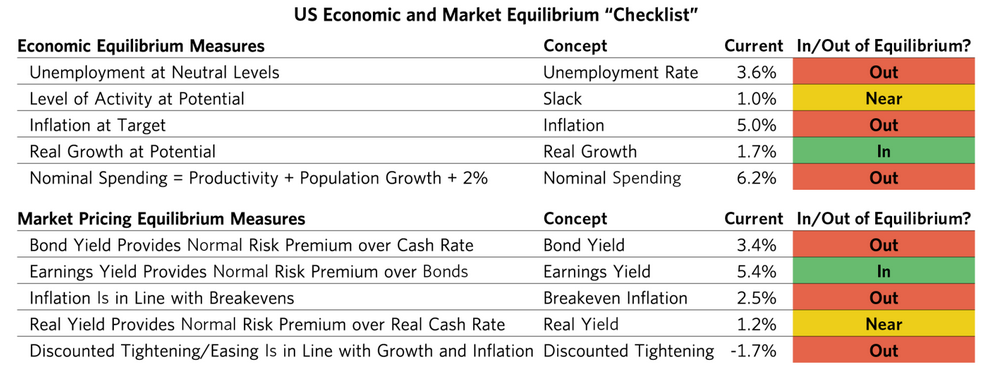

“The greatest disruption of equilibrium today remains the high level of nominal spending, which, when compared to the ability of the economy to produce more, leads to inflation rates that are significantly above target....

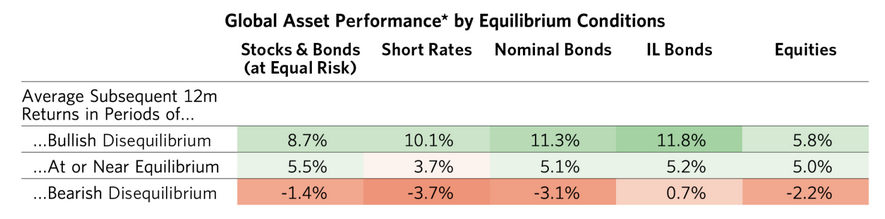

“We are now in the bearish disequilibrium. The following table summarizes a few key measures for the U.S. economy. With respect to the economy, the inflation rate is too high, the rate of nominal spending is too high to bring that down, the rate of unemployment is too low to bring wages down….

“Bond yields are too low in relation to cash and discounted inflation rates are well below current and projected inflation rates, so there is no risk premium in bonds…. At the same time, nominal spending is too high and the labor markets are too tight to allow for the easing of policy that is priced into the front of the yield curve, which is the easing that would be necessary to provide for a normal risk premium in bonds.”

Please see below:

To explain, when nominal spending, inflation and employment are out of whack with economic normality (bearish disequilibrium), bond yields need to rise to create the demand destruction necessary to suppress inflation. And the shaded red areas above show how nominal bonds suffer during these periods.

Conversely, the crowd is pricing in rate cuts. And while this helps uplift the PMs, the optimism contrasts fundamental reality. Likewise, Bridgewater Associates highlights how most of its economic and market-pricing metrics remain in bearish disequilibrium (the shaded red areas).

Please see below:

How Do We Achieve Equilibrium?

To rid the U.S. economy of its inflation problem, achieve the rate-cuts/QE priced in by investors, and end the PMs’ rolling bear markets, wages and consumer spending need to decline materially, which is not happening right now. The CIOs continued:

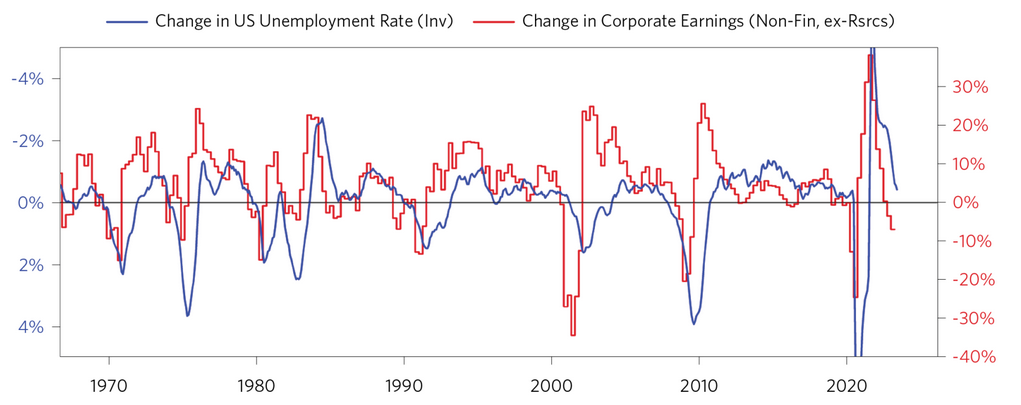

“Nominal spending, fueled by the wages that consumers earn, is running close to 8%, above the roughly 5% in the recent decades of subdued inflation…. The spread between nominal spending and wages is a good proxy for economy-wide corporate profits, and that positive spread incentivizes hiring and additional wage pressure….

“We estimate corporate profits need to fall roughly 20% and are currently down a bit less than 10%. More pain is needed to raise unemployment, reduce wages, and moderate inflation.”

Please see below:

To explain, the red line above tracks the percentage change in U.S. corporate earnings (excluding financials and resources), while the blue line above tracks the inverted (down means up) percentage change in the U.S. unemployment rate.

If you analyze the relationship, you can see that ~20% declines in corporate earnings have often been required to induce layoffs, raise the unemployment rate (falling blue line), moderate wage inflation, and eradicate output inflation. Yet, we are far from this level of demand destruction, and the PMs have benefitted from the fundamental naivety.

Overall, while the permabulls remain highly confident, you can’t run from reality. And if growth, employment, and inflation don’t slow fast enough, interest rates will need to rise, which is bullish for the USD Index and bearish for the PMs. As such, we expect these issues to haunt the paper silver price in the months ahead.

Do you agree or disagree with Bridgewater Associates’ conclusions?

********

share

share

share

share

share

Alex Demolitor hails from Canada, and is a cross-asset strategist who has extensive macroeconomic experience. He has completed the Chartered Financial Analyst (CFA) program and specializes in predicting the fundamental events that will impact assets in the stock, commodity, bond, and FX markets. His analyses are published at GoldPriceForecast.com.

Alex Demolitor hails from Canada, and is a cross-asset strategist who has extensive macroeconomic experience. He has completed the Chartered Financial Analyst (CFA) program and specializes in predicting the fundamental events that will impact assets in the stock, commodity, bond, and FX markets. His analyses are published at GoldPriceForecast.com.

More from Silver Phoenix 500