US Dollar slips back to 104.00 as NFP looms

NEW YORK (August 2) The US Dollar (USD) maintains its offered stance well in place so far in the European session, approaching the 104.00 neighbourhood when tracked by the USD Index (DXY). That said, the index gives away part of Thursday’s marked advance, although it keeps unchanged the range-bound trade seen in the past couple of weeks.

In fact, the Greenback managed to set aside part of the post-FOMC weakness on Thursday, after further cooling of the domestic labour market (as per weekly Jobless Claims) and a disenchanting print from the ISM Manufacturing Purchasing Managers Index (PMI) for July (46.8) reignited fears of a potential slowdown in the US economy, jeopardizing the view of a soft landing following the hiking cycle by the Federal Reserve (Fed)

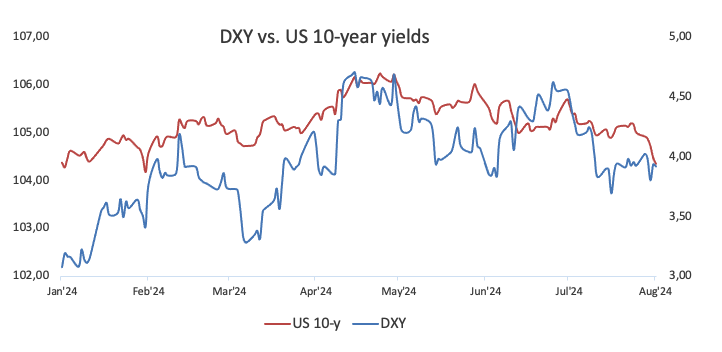

In addition, the resurgence of geopolitical jitters, especially in the Middle East, favoured the demand for the safe haven US Dollar, which in turn kept the risk-linked complex depressed. The incessant move lower in US yields across different time frames also reinforced the flight-to-safety sentiment.

Moving forward, the FX universe is expected to enter the usual pre-NFP lull around current levels, while the outcome of the jobs report should have a temporary impact on bets around a September interest rate cut.

Absent an FOMC event this month, market participants and the Fed will have two inflation prints and two more labour market reports to further evaluate the likelihood, or not, of an interest rate reduction beyond the summer.

Despite the Fed Chair Jerome Powell's dovish message on Wednesday, opening the door to lower rates in September, the statement of the central bank reiterated that further confidence that inflation is heading towards the 2% target is needed to start an easing cycle.

Daily digest market movers: The Dollar keeps the offered bias ahead of Payrolls

- A firm bounce in the risk complex puts the US Dollar under pressure.

- The US economy is expected to have created 175K jobs in July.

- The US Unemployment Rate is seen holding steady at 4.1% last month.

- Factory Orders will also be under scrutiny amidst renewed slowdown concerns.

- Yields maintain their firm downtrend and navigate multi-week lows across different maturity periods.

- Unabated geopolitical concerns in the Middle East remain a source of strength for the Greenback for the time being.

- CME Group’s FedWatch Tool continues to fully price in lower rates in September.

Short-term technicals on the US Dollar

The US Dollar Index (DXY) maintains the trade around the key 200-day Simple Moving Average (SMA) at 104.29. A convincing breakdown of this region should leave the index vulnerable to extra losses in the short-term horizon. That said, initial support emerges at the July low of 103.65 (July 17), prior to the weekly low of 103.17 (March 21) and the March bottom of 102.35 (March 8).

Bouts of strength, on the other hand, face an interim barrier at the 55-day and 100-day SMAs at 104.83 and 104.91, respectively, ahead of the June top of 106.13 (June 26). Once the latter is cleared, DXY could attempt a move to the 2024 peak of 106.51 (April 16).

FXStreet